Walmart & Synchrony Partner; Chime IPOs; Oportun’ $439Mn Securitization

Core inflation came in at 2.8%. Octaura raises $46.5Mn. Parlay announces seed funding. Walmart and OnePay partner with Synchrony. Oportun completes $439Mn securitization. Sezzle sues Shopify. Chime IPOs.

We’re launching RfP to close payments' speed gap — while payouts have become instant, pay-ins still rely on slower traditional ACH rails. RfP brings both sides into real-time. Plaid is our first partner to use RfP for real-time vehicle purchase funding. Catch up with more on this here.

In case you missed it, we published our Q1 Consumer Lending Review this week. Read the full report here.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

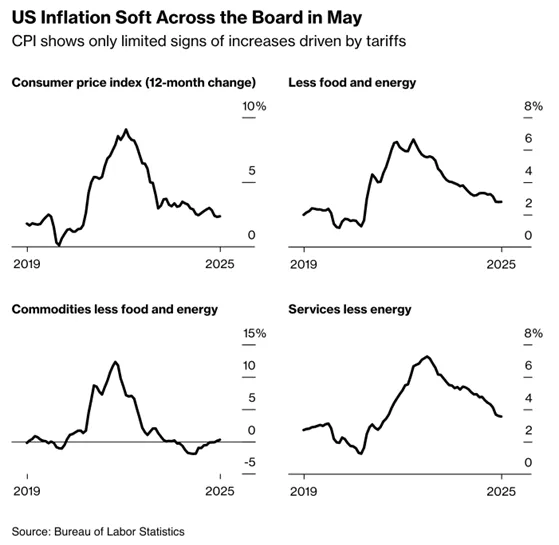

Core Inflation at 2.8%

The most recent CPI print came in somewhat better than expected, showing core inflation, which excludes more volatile food and energy prices, rose 0.1% in May vs. April. Year over year increase in core inflation came in at 2.8%. Clothing and new and used automobile prices declined, while services prices, excluding energy, rose 0.2%. Lower-than-expected inflation numbers may be hard for consumers to reconcile with some of the “sky is falling”-type coverage of President Trump’s on-again, off-again tariffs, which, economists warn, risk exacerbating price hikes and potentially even leading to shortages of some imported goods. Although inflation has remained somewhat subdued for the time being, given the ongoing uncertainty around Trump’s tariff policies and a steady labor market, the Fed is expected to hold rates steady at its next meeting.

Octaura Raises $46.5Mn

Octaura, a loan syndication platform, has announced it has raised $46.5Mn in new funding. Investors in the round include existing investors Wells Fargo, Citi, JPMorgan, Bank of America, Moody’s and Wells Fargo, as well as new investors BNP Paribas, Deutsche Bank, Barclays, Apollo, Motive Partners, Mass Mutual Ventures, and Omers Ventures. The heavy interest from banks makes sense, as Octaura was founded in 2022 by a consortium of banks to create a market for trading collateralized loan obligations and syndicated loans. The platform launched in 2023 and has, since then, grown its dealer network from three to 25 and expanded buy-side participants from 34 to 146 companies. Octaura’s platform now accounts for 4.6% of the volume of the secondary trading market. Octaura CEO Brian Bejile said, “Octaura was created to improve the availability and use of data and analytics solutions for the loan and structured credit markets,” which gives market participants better, more streamlined accessibility with fewer errors.

Parlay Announces Seed Funding

“Loan intelligence system” startup Parlay announced it has raised $2Mn in seed funding. The round was led by JAM FINTOP. Parlay’s offering helps lenders improve their operational efficiency, thereby boosting loan volume and increasing profitability, without taking additional credit risk. Parlay’s loan intelligence system works with lenders’ existing loan origination systems, offering features that include customer onboarding, data verification, decision management, which are particularly well-suited for complex use cases, like underwriting Small Business Administration loans. Speaking on the news, Parlay cofounder and CEO Alex McLeod said, “JAM FINTOP’s investment and network of banks creates a powerful multiplier effect for our technology. Through this partnership, we’re empowering community lenders nationwide to maintain rigorous underwriting standards while drastically improving operational efficiency and insight. By democratizing access to AI-powered technology, Parlay is helping community banks to better compete while advancing their mission to serve local businesses.”

Walmart and OnePay Partner with Synchrony for Cobrand Cards

Everything that’s old is new again, it seems. Walmart, which partnered with Synchrony to issue its cobrand cards before moving the program to Capital One, until the two parted ways, ostensibly stemming from a contract dispute in 2023. It was widely viewed at the time that Walmart was leveraging the disagreement over Capital One meeting certain service level agreements to move its cobrand program to OnePay, the fintech Walmart is a majority owner of. And, indeed, that’s what Walmart has done. OnePay will begin issuing Walmart general purpose and private label credit cards starting later this year, with Synchrony serving as the bank sponsor. The move is OnePay’s latest to build beyond its checking account/debit card product to offer additional credit programs. In March, the company announced a partnership with Klarna to underwrite longer-term, interest-bearing loans, and OnePay has offered a credit builder product for some time now as well.

Oportun Completes $439Mn Securitization

Non-bank lender Oportun has completed a $439Mn asset-backed securitization. The two-year revolving fixed-rate notes are backed by pools of secured and unsecured consumer loans issued by Oportun. Oportun will pay a weighted average coupon across tranches of 5.57%, with “Class A” notes priced as 4.88% per year. Oportun interim CFO Paul Appleton said of the transaction, “This transaction marks an important milestone for Oportun and reflects a growing recognition of the strength and resilience of our business. Achieving our first AAA rating demonstrates how far we’ve come in expanding access to affordable credit.”

Sezzle Sues Shopify

Sezzle is suing Shopify, arguing the ecommerce platform is violating antitrust laws by favoring its own BNPL offering over third parties’. Sezzle alleges in its suit that Shopify’s BNPL program takes more than 75% of the volume on Shopify’s platform, three years after Shopify launched its own BNPL capability to compete with third parties like Sezzle. Shopify also imposed penalty fees on merchants who used Sezzle or other non-Shopify BNPL providers, Sezzle claims in its suit.

Chime Raises $864Mn in IPO

Chime investors should be happy, most of them anyway. The company ended up pricing its IPO at $27 per share, selling 32Mn shares to raise a total of $864Mn. When trading began on Thursday morning, Chime’s price per share jumped to $43. Chime’s shared ended the day at about $37, or a 37% pop from its IPO price, valuing the company at about $13.5Bn. Still, Chime was once valued at as much as $25Bn, meaning some late-stage investors may still be underwater.