FOMC Minutes; Circle Plots IPO; Are PFMs Back?

FOMC meeting minutes. NCUA layoffs. Are PFMs back? Circle plots IPO. Global Payments divests payroll unit. Revolut profit jumps. Starling profit declines.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

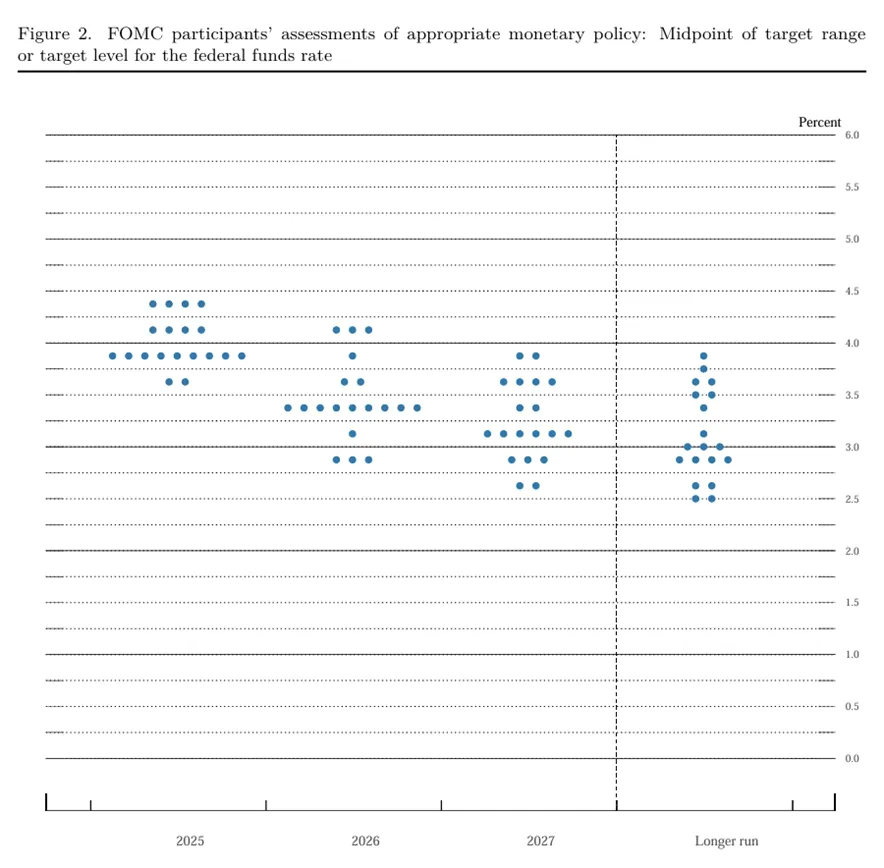

FOMC Minutes

The Fed justified its cautious approach on rates, recently released minutes from the last FOMC meeting show. Policymakers were broadly aligned that continued economic uncertainty and inflation that remains elevated require more time and data before making any decision to cut rates. The minutes show that concerns about inflation and unemployment have both increased since the last FOMC meeting. “Participants agreed that with economic growth and the labor market still solid and current monetary policy moderately restrictive, the committee was well positioned to wait for more clarity on the outlooks for inflation and economic activity,” according to minutes of the meeting.

NCUA Layoffs

The NCUA, which provides deposit insurance coverage to and oversees the nation’s credit unions, is planning to trim headcount by 20% by the end of the year, acting NCUA Chair Kyle Hauptman confirmed at a board meeting last month. The voluntary separation initiative, consisting of a deferred resignation option and an early retirement incentive, were developed in alignment with Trump’s executive order implementing the DOGE “workforce optimization” initiative. The reductions would amount to more than 200 workers at the agency. Hauptman said the restructuring would reduce costs on credit unions and enable longer-term operational reform. NCUA is the latest financial regulator to announce an effort to shed workers. The FDIC, OCC, and Federal Reserve have all floated plans to reduce headcount at their respective agencies.

Monarch Raises $75Mn Series B

Personal financial management apps, of which Mint (RIP) is probably the best known, were an early darling of the fintech “1.0” era. And while they demonstrated an early use case for open banking, product/market fit was generally limited to a subset of finance optimizers, and didn’t achieve the kind of breakout success that other early product categories, like peer-to-peer payments, had. There were also business model challenges. With most consumers averse to pay for such services, first-gen PFMs typically monetized through advertising, by referring customers to offers for loans, credit cards, bank accounts and the like. There was also little moat to protect early PFMs from banks copying their capabilities and rolling them out as features of their existing checking and savings accounts, though with limited uptake.

Monarch, founded in 2018 and led by a one-time director of product at Mint, announced it has raised a $75Mn Series B that values the company at $850Mn. The round was co-led by Forerunner Ventures and FPV Ventures, with participation from existing investors Menlo Ventures, Accel, SignalFire, and Clocktower Ventures. Monarch notably does charge a monthly fee: $14.99 per month, or $8.33 per month if paid annually. After Mint’s shutdown, Monarch saw a 20x jump in subscribes, Monarch cofounder and CEO Val Agostino recently told CNBC.

Circle Plots IPO

USDC stablecoin issuer Circle seems to be trying to strike while the iron is hot. The company attempted to go public via a SPAC deal in 2022, which would have valued it around $9Bn. Now, the company is targeting a price of $24 to $26 per share in an IPO that would raise about $624Mn, according to paperwork the company filed with the SEC last week. According to Bloomberg’s analysis, pricing at the top of the range would value Circle at about $5.65Bn, or around $6.7Bn on a fully diluted basis that accounts for stock options and restricted share units in the company. Circle has benefited from higher rates, as nearly all of its revenue is generated from reserve assets it holds. The company posted net income of $156Mn on revenue of $1.68Bn in 2024, its filings show.

Global Payments Divests Payroll Unit

Global Payments is divesting from its payroll processing unit, selling the business to Acrisure for $1.1Bn, it said in a press release last week. Acrisure said it plans to rebrand the unit, currently known as Heartland Payroll Solutions, after the deal closes, which is expected to be sometime in the second half of this year. The move comes as Global Payments works to continue to sharpen its focus by divesting non-core businesses. Earlier this year, the company sold its issuer business to Fidelity National Information Services for $13.5Bn and sold a healthcare unit to an investment firm for $1.1Bn.

Revolut Profit Jumps, as Starling’s Declines

U.K.-based Revolut saw its revenue jump 72% last year to about $4Bn, the company’s just-released financials show. Profit before taxes reached $1.4Bn, with net income more than doubling to about $1Bn vs. $428Mn the year prior. Revolut reported a total of 52.5Mn users across its four main business lines: card payments, foreign exchange, subscriptions, and wealth management.

Meanwhile, fellow British neobank Starling, which primarily serves SMB customers, saw its profit decline, owing to a fine to the country’s regulator, the FCA, and rising delinquencies on COVID-era loans. Starling paid £29Mn in fines for failures related to its sanctions screening practices. Starling also recorded a £28.2Mn provision for loan losses after correcting a previous error related to government guarantees for loans to smaller business during the pandemic. Still, it wasn’t all bad news for the bank. Starling did see customer deposits jump by over £1Bn, from £11Bn to £12.1Bn.