Fed Cuts Rates; U.S. Retail Sales Rose; Plaid & JPMC Reach Fee Deal

.png)

The Fed cut rates by a quarter point. U.S. retail sales rose, while credit scores are dropping on average. Lendbuzz files to IPO. Stablecore, WorkFusion, Arch, and SEON all announce new funding. Plaid and JPMorgan Chase reach fee deal in open banking fight.

Just launched! Advanced Authorization by Cross River puts fintechs in control of real-time card approvals—custom logic, fewer improper declines, and faster innovation, all backed by our banking rails and compliance infrastructure. Learn more.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

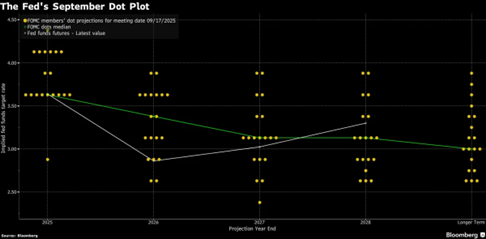

Fed Cuts Rates By 25bps

The Federal Reserve cut its benchmark interest rate target by 25bps at last week’s Federal Open Market Committee meeting. The meeting was even more closely watched than normal, if that’s possible, with the controversy over Fed Governor Lisa Cook continuing to play out and President Trump’s pick to replace Governor Adriana Kugler, Stephen Miran, joining his first rate setting meeting. Miran was the sole dissent, voting for a larger 50bps rate cut. The Fed indicated it expects to cut rates twice more this year, with Fed Chair Powell pointing to increasing signs of softness in the U.S. labor market.

Meanwhile, U.S. retail sales rose for the third month in a row in August. Total value of retail purchases, not adjusted for inflation, increased by 0.6% month over month in August, after posting a similar gain in July. Growth was fairly widespread, with nine out of 13 categories posting sales increases. However, it’s increasingly the richest Americans who are driving consumer spending. Consumers in the top 10% of income accounted for nearly half, a whopping 49.2%, of total spending in the second quarter. Finally, consumers are seeing their credit scores drop at the fastest rate since the Great Recession. The national average FICO score dropped by two points this year, according to data released by the company last week.

Lendbuzz Files For IPO

When it rains, it pours… with no one certain how long the IPO window will remain open, more companies are rushing to make their public debuts. The latest, Lendbuzz, an auto lender, filed its S-1 registration statement with the SEC last week. The company uses artificial intelligence to underwrite vehicle loan applicants, with a focus on borrowers with limited credit histories. The company hasn’t yet set a number of shares or price target for the offering. JPMorgan, Goldman Sachs, Mizuho, and RBC Capital Markets are serving as lead booker runners on the deal, which will see Lendbuzz list on the Nasdaq under the ticker “LBZZ.”

Stablecore Raises $20MM

Stablecore, a technology platform that enables community and regional banks to offer their own stablecoins, tokenized deposits, and digital asset products announced it has raised a fresh $20MM in funding. The round was led by Norwest, with participation from Coinbase Ventures, BankTech Ventures, Curql, Bankers Helping Bankers Fund, EJF Ventures, and Bank of Utah. The platform serves as a “digital asset core,” analogous to financial institutions’ core banking systems typically provided by vendors like FIS, Fiserv, and Jack Henry. Stablecore is designed to integrate with institutions’ existing core and digital banking systems.

Alex Treece, cofounder and CEO of Stablecore, commented on the fundraise by saying, “Following landmark regulatory changes this year, stablecoins and digital assets have entered a new paradigm, becoming permissible activities within banking. Banks and credit unions - especially Main Street institutions - are the most logical, secure home for these assets alongside customers’ existing financial accounts. Stablecore helps financial institutions retain their deposits, create new digital asset-powered revenue streams and stay competitive as this transition to digital assets and blockchain technology unfolds.”

WorkFusion Bags $45MM in New Funding

WorkFusion, a startup developing AI agents for financial crime compliance, announced it has raised $45MM in new funding, Crunchbase News is reporting. The company, founded in 2010, originally focused on intelligent document processing and process automation, but pivoted to focus on financial crimes compliance a few years ago. The company repackaged its existing models as AI agents, even assigning these agents names and job titles, to help financial institutions more easily understand their capabilities. Agents can perform compliance functions that include sanctions screening alert reviews, transaction monitoring investigations, adverse media screening, KYC refreshes, enhanced due diligence, and fraud alert reviews. Georgian led the investment round, with participation from Hawk Equity, Teralys Capital, NGP Capital, Serengeti Asset Management, and others. The company plans to use the proceeds to make strategic hires as it continues building out and scaling its platform

Arch Raises Series B

Wealthtech firm Arch announced it has raised a $52MM Series B. The financing round was led by Oak HC/FT, with participation from Menlo Ventures, Quiet Capital, and Craft Ventures. Arch offers an AI-powered platform for managing private and alternative investments. The company caters to family offices, fund administrators, and registered investment advisors by offering capabilities that include document management, data processing, and workflow automation. Arch cofounder and CEO Ryan Eisenman commented on the news, saying, “With this new capital and the support of our partners, we’re expanding our suite of CIO tools, developing new features within our client portal and enhancing reporting capabilities for limited partners.”

SEON Announces $80MM Series C

Fraud screening startup SEON announced it has raised an $80MM Series C. The round was led by Sixth Street Growth, with participation from Firebolt, IVP, and Creandum. As part of the new investment, Sixth Street Growth principal Claire Zhang will join SEON as a board observer. SEON’s API-based platform leverages over 900 proprietary data signals for fraud screening, AML compliance, and customer verification. Customers include heavyweight names in fintech like Plaid, Nubank, Afterpay, and Revolut. SEON plans to use the new funding further develop the capabilities of its platform and to deepen relationships with existing financial institutions and cloud service providers.

Plaid and JPMorgan Chase Reach Fee Deal

In the latest dramatic move in the battle for open banking, data aggregator Plaid has agreed to pay JPMorgan Chase for accessing its customers' data, Bloomberg reported last week. The seeming detente modifies an existing bilateral data sharing agreement between Plaid and the bank. Both parties confirmed that Plaid would begin paying for access, but declined to specify details about the size or structure of the charges. Bloomberg also reported that the deal reached between Plaid and JPMorgan Chase derailed a planned lawsuit against the bank from industry trade group FDATA over the fee plan, but that the group is now reconsidering potential litigation.