CFPB Drops Consent Orders; Miran Pushes Lower Rates; Is Tether Worth $500Bn?

.png)

Fed’s Miran says rates should be lower. Powell says asset prices high, but financial stability risks not elevated. CFPB drops consent orders as it runs out of money. FinWise data breach. FIS acquires amount. PayNearMe, Cardless raise new funding. Tether seeks to raise up to $20Bn at $500Bn valuation (yes, you read that correctly).

We’re excited to be heading to Money20/20 next month. If you’ll be there, let’s connect and explore what we’re building—and what’s next in fintech. Book a meeting.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

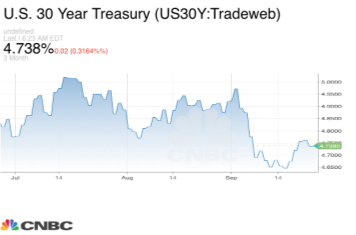

Miran Says Fed Benchmark Should Be 2.5%

Recently confirmed Federal Reserve Governor Stephen Miran said he thinks the central bank’s benchmark interest rate should be significantly lower than its current level in remarks he made last week to the Economic Club of New York. Miran argued that the rate should be closer to 2.5%, almost a full percentage point lower than any of his fellow 18 members of the Fed’s rate setting committee. Miran was the sole dissenting vote at the Fed’s most recent FOMC meeting, voting for a half-point cut, while the other 11 voting members agreed on a quarter-point cut. Despite that quarter-point cut, 10- and 30-year Treasury yields rose, hitting 4.145% and 4.76%, respectively. A rise in longer-term yields is likely to impact consumer lending rates that reference Treasuries as a benchmark, including auto and mortgage loans.

Miran’s outspokenness, particularly as his views deviate significantly from other FOMC members, is a break with the normally consensus-driven institution. In other Fed-related news, Fed Chair Powell said last week that asset prices are elevated, commenting that, “We do look at overall financial conditions, and we ask ourselves whether our policies are affecting financial conditions in a way that is what we’re trying to achieve. But you’re right, by many measures, for example, equity prices are fairly highly valued.” However, Powell said that, despite elevated asset prices, he did not view financial stability risks as elevated.

CFPB Drops Consent Orders

The Consumer Financial Protection Bureau is expected to drop all pending enforcement actions, employees told American Banker, as the Bureau is expected to run out of funding and is looking to terminate or furlough staff. The American Banker report comes amid news that the CFPB opted to end consent orders entered into by Apple and U.S. Bank early. Both Apple and U.S. Bank paid penalties related to their enforcement actions, regarding the launch of the Apple Card and unemployment benefit restrictions, respectively. The early termination of their consent orders frees the companies from enhanced compliance requirements and ongoing monitoring years earlier than would have otherwise been the case. In a court filing terminating the U.S. Bank order, acting CFPB Director Russ Vought said U.S. Bank had fulfilled certain obligations under the order, that the bank was taking steps to prevent future violations, and that the Bureau “also waives any alleged noncompliance therewith.” Similarly in the Apple matter, the Bureau waived any “alleged noncompliance” with the now-terminated consent order.

FIS Acquires Amount

Core banking provider FIS is acquiring deposit and loan origination platform Amount, the companies announced last week. Amount was spun off from lending startup Avant in January 2020 and was valued at as much as $1Bn in 2022. Terms of FIS’ acquisition of Amount were not disclosed. Amount serves banks and credit unions with an aggregate of $3.1Tr in assets and 50MM customers. FIS CEO Stephanie Ferris commented on the deal, saying, “After years of successful partnership, we are thrilled to welcome Amount’s talented team and innovative capabilities to FIS.” Amount CEO Adam Hughes added, “FIS provides global scale, robust infrastructure and regulatory expertise that will allow us to strengthen our market offering and deliver seamless, innovative customer experiences and accelerate digital transformation.”

PayNearMe Raises Series E

PayNearMe announced it has raised a $50MM Series E from Atlantic Vantage Point. PayNearMe offers what the company calls “Payment Experience Management,” consisting of a combination of its proprietary software and money movement capabilities. The company plans to use the new funding to continue investing in products that streamline end-to-end payments experiences and to expand into new markets. Commenting on the new funding, PayNearMe CEO Danny Shader said, “For too long, payments have been treated only as a cost of doing business. We see improving payments as a powerful opportunity to help businesses differentiate, drive customer satisfaction, and improve business results. AVP's funding will allow us to deliver the benefits of Payment Experience Management to more clients and in new markets.”

Cardless Bags $60MM

Cobrand card platform Cardless announced it has raised another $60MM in capital, bringing its total funding to date to $170MM. The round was led by Spark Capital, with continued support from Activant Capital, Pear VC, Industry Ventures, and others. Cardless customers include Coinbase, Alibaba, Qatar Airways, and Bilt Technologies. As of Q2, Cardless says it has about $15MM in annualized revenue and is projecting 10x revenue growth by Q2 2026. The company plans to use the new funding to continue growing its existing cobrand programs and to develop and launch new ones. Cardless cofounder and president Michael Spelfogel commented on the news, saying, “If you have a co-branded card today with Amazon or Costco or Marriott, you probably go to that bank’s app to manage your card. We build infrastructure to enable those brands to put their credit card directly in their ecosystem, which decreases friction, increases conversion and, ultimately, makes the brand more money.”

Tether Seeks To Raise at Eye-Popping $500Bn Valuation

Tether, the issuer of the stablecoin by the same name, is reportedly seeking to raise as much as $20Bn in new funding at a valuation that could reach an eye-popping $500Bn, potentially making the company one of the world’s most valuable private firms. Bloomberg reported that Tether is trying to raise between $15Bn and $20Bn by selling a 3% stake in the company through a private placement. As a point of comparison, publicly traded Circle, which issues the USDC stablecoin, currently has a market capitalization of just north of $30Bn. The outsized valuation is a bit of a headscatcher, though. Ostensibly, the company’s business model amounts to issuing “tethers” (stablecoins), which are not interest-bearing, and holding the backing assets, collecting the yield on those reserves for itself. While high margin, it also makes for an extremely interest rate sensitive business, precisely at the moment that interest rates are declining.