Q4 2025 Review | Consumer Lending

.png)

Hi all, Cole here

We come to you today with our quarterly consumer lending review. Catch up on the latest trends in the consumer lending space:

- takeaways from nonbank and bank earnings:

- originations (personal loan, BNPL, cash advance, high APR, second look, LTO)

- credit data (BNPL, cash advance, nonbank, bank)

- and an increase in MPL new issue volume

New here? Subscribe to receive our newsletter each Sunday.

Missed last quarter’s report? Catch up on key trends with my Q3 Consumer Lending Review.

Consumer Loan Originations Roll On

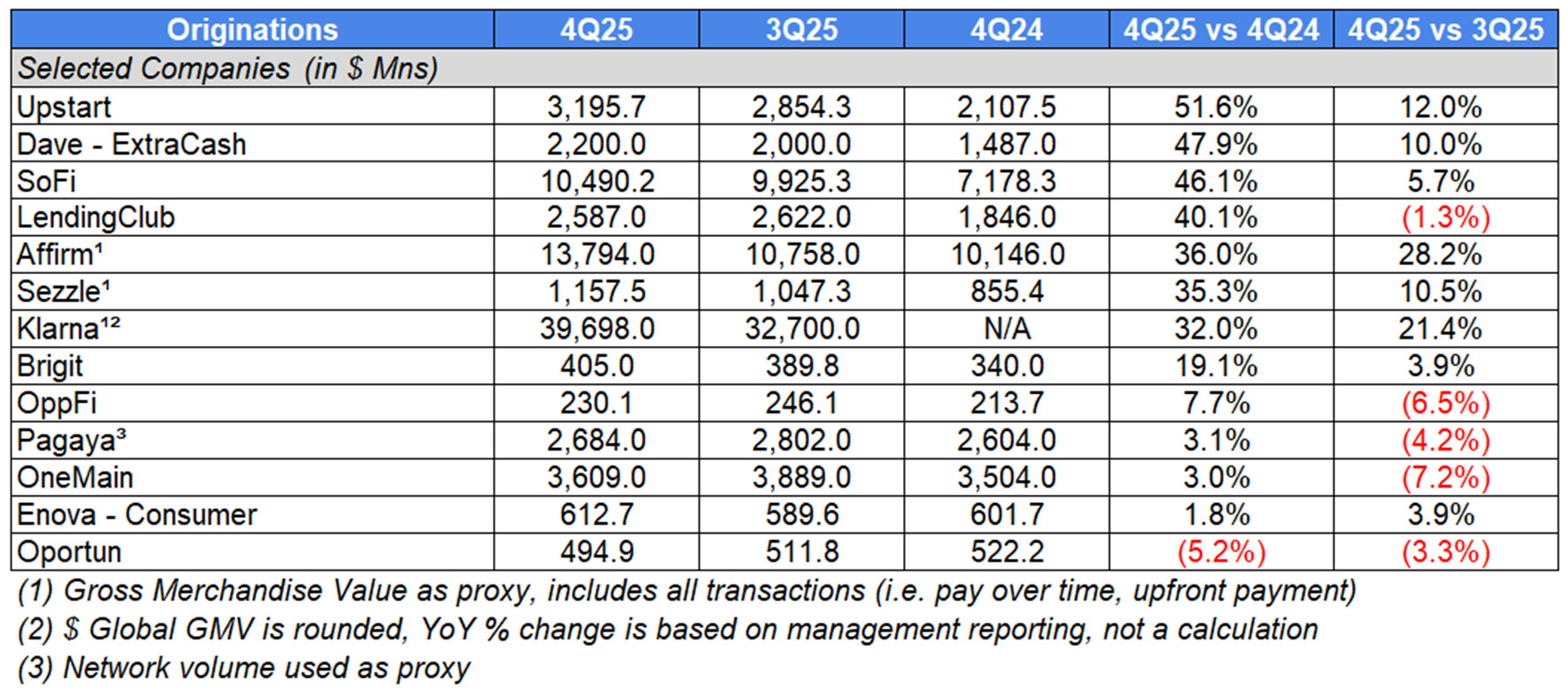

Originations

In the fourth quarter, lenders continued to report strong YoY growth in originations across lending products (BNPL, cash advances, higher-APR (36%+ APR) loans, personal loans). Consumer demand for credit remains strong, with aggregate household debt hitting a record high of $18.78Tn in Q4, per New York Fed data.

Personal Loan-Focused

Following the two-year period (mid-2022 to mid-2024) of declining/tepid growth in originations due to credit tightening efforts, unsecured personal loan volume continued to rebound.

Upstart reported +52% YoY growth in originations, led by super prime (720+ credit score) originations, which were up +74% to $786Mn. Super prime originations represented 27% of all personal loan originations, up from 22% a year prior. Additionally, Upstart reported strong growth in its small-dollar originations, which were up +50% YoY to $111Mn, and its auto originations, which were up +344% YoY to $200Mn.

Upstart recently joined the wave of fintechs pursuing charters, applying to the OCC and FDIC to establish an insured national bank. If approved, holding a charter and being able to take insured customer deposits would reduce Upstart’s operational, regulatory, and financial costs, the company says. Paul Gu, Upstart’s CTO, commented on the decision to apply for a charter, saying, “The time is right to launch the first bank built from the ground up on AI. Applying for a bank charter is the natural evolution of our business as we’ve grown in size, scale, and product offerings. This will allow us to save borrowers even more time and money, and streamline our partnerships with banks, credit unions, and institutional credit funds.”

SoFi reported strong origination growth, up +46% YoY, fueled by borrower demand across asset classes. SoFi launched the SoFi Smart Card in Q4, a charge card secured by SoFi Checking and Savings that offers enhanced rewards at grocery stores and aims to help consumers grow their credit scores.

In Q4, SoFi continued to invest in the crypto space. SoFi launched crypto trading for consumers and launched its own stablecoin, SoFiUSD. It plans to offer additional products and services in 2026, including lending secured by crypto, institutional trading and correspondent payments and settlement via stablecoins.

LendingClub management attributed its +40% YoY origination growth to product innovation, loan investor demand, and increased marketing efforts. Origination growth was led by marketplace loan originations, which were up +68% YoY. LendingClub reported strong traction for its LevelUp Savings and Checking products, with double digit growth in accounts YoY. The company continues to work towards its planned entry into the home improvement financing market, and is on track to launch midyear.

OneMain posted a more modest +3% YoY increase in originations, even as the company maintains tighter credit standards and higher pricing. However, the company expects room for growth, as it introduces a new secured lending product for homeowners. In March 2025, OneMain filed an application with the Utah Department of Financial Institutions and the FDIC to form OneMain Bank (an industrial loan company). Management said it has continued to make progress but does not have a timeline yet. Once/if it receives approval, it expects about a year to operationalize and see positive results from the charter.

Origination growth has been helped by its credit card business. OneMain continued to gain traction with its BrightWay credit cards, growing receivables +46% YoY to $936Mn.

Oportun originations declined (5)% YoY, after four straight quarters of YoY growth, as the lender realized effects of its Q3 credit tightening efforts. Despite this, Oportun’s secured personal loan product has continued to thrive, with receivables growing +39% YoY to $226Mn, to reach 8% of its owned portfolio balance. Oportun’s secured personal loans allow borrowers to secure their loans with their car titles, potentially allowing access to larger loans at lower rates than an unsecured loan. These loans have seen significantly better credit performance with the secured NCO rate ~600bps lower than the unsecured NCO rate through 2025. Additionally, these loans generate 2x the revenue per loan compared to unsecured personal loans, primarily due to higher average loan sizes.

Notably, Oportun announced that it is exploring the reintroduction of risk-based pricing above 36% APR for select higher-risk segments on shorter-term loans. Currently, Oportun does not lend above 36%. If it reintroduces this pricing, Oportun would work with new bank sponsors (currently working with Pathward) and warehouse providers.

BNPL-Focused

BNPL growth isn’t slowing down, with the category’s success driven by increased market penetration and increased usage by consumers. An increasing number of BNPL players are seeking banking charters.

Affirm’s YoY GMV (gross merchandise volume) growth of +36% benefited from a more engaged user, with 6.4 transactions per active consumer, up from 5.3 a year prior. At the same time, its average order value declined (6)% YoY to $251, in-line with strategy. GMV growth was led by 0% APR products, with its 0% APR Monthly products +65% YoY and Short-Term 0% APR +55% YoY. Its interest-bearing product grew +27% YoY. The Affirm Card continues to scale, with 3.7Mn active cardholders at quarter end, up +121% YoY and card GMV of $2,186Mn, up +159% YoY.

In January, Affirm filed applications to form a Nevada industrial loan company and a corresponding application for FDIC deposit insurance. The charter would enable Affirm to raise its own deposits, lowering its cost of funding vs. current channels, such as securitizations. Affirm cofounder and CEO Max Levchin commented, saying, “A banking subsidiary would strengthen and diversify Affirm's platform, and help us bring honest financial products to more people. This is about expanding what we can do for consumers and merchants, and building for the long term.”

Sezzle’s +35% YoY growth in GMV was also driven by greater usage of subscription products and increased consumer engagement. Quarterly purchase frequency rose to 6.6x, up from 5.5x a year prior.

Sezzle is exploring an ILC (industrial loan company) charter and disclosed that it is in the discovery phase supported by external consultants and attorneys. Management indicated that it anticipates submitting an application in the first half of 2026. Currently, Sezzle partners with WebBank to offer its financial products.

Zip Co, a BNPL provider that operates in the U.S., Australia, and New Zealand, reported FY1H26 results, with a +34% increase in volumes. For context, roughly three-quarters of its volumes come from the U.S. market, which grew +45% YoY. In February, Zip’s U.S. business rolled out a “Pay-in-2” installment solution to all customers, building on its product offerings, which include a Pay-in-8 option.

Klarna reported +32% GMV growth YoY, helped by a +43% increase in U.S. GMV. Klarna’s Fair Financing (typically a 6-12 month term product which may charge interest) volumes soared, up +165% YoY. 20% of Klarna merchants now offer Fair Financing, up from 18% in Q3. Klarna said its Fair Financing offering has a transaction margin over 2x the group average.

Klarna Card continued to gain traction during its rollout, posting 4.2Mn active users in Q4. The Klarna Card accounted for over 15% of total transactions, and GMV was up +209% YoY.

Wrapping things up, PayPal reported strong growth in its BNPL TPV, which exceeded $40Bn in FY2025, a +20% increase YoY. Additionally, PayPal filed applications to establish a Utah-chartered industrial loan company. PayPal said that the charter would help it provide lending solutions more efficiently to small businesses in the U.S.

Cash Advance-Focused

Consumers looking for a way to bridge the gap between paychecks have increasingly turned to earned wage access and short-term cash advance products.

Dave reported a +48% YoY increase in originations, driven both by the size of originations (+20% YoY to $214) and by growth in monthly transacting members (+19% YoY to 2.9Mn). At the same time, Dave has continued to grow its average revenue per ExtraCash advance, which grew +33% YoY to $13.5.

Dave is also exploring new product offerings. The cash advance player is working to add a BNPL product, which is currently in internal testing. It expects to begin customer testing soon but doesn’t expect meaningful Pay-in-4 revenues in 2026, as it remains focused on optimizing unit economics before scaling in 2027. More than half of Dave members engage in some form of BNPL transaction and Dave has access to significant member cash flow and underwriting data. With the move into BNPL, Dave will be entering a market dominated by mature players such as Affirm, Afterpay, Klarna and PayPal.

Brigit has reported strong growth since being acquired by Upbound Group, with volumes growing +19% YoY. Brigit grew its average revenue per user +10% YoY to $14.15 on higher expedited transfer fees, deeper engagement with marketplace offers, and a shift toward the Premium tier.

Brigit began to pilot its line of credit product in late 2025. The product offers up to $500 of liquidity on recent or upcoming purchases, twice the cap on its Instant Cash advances. Management aims for the product to bridge the gap between smaller ticket BNPL and larger ticket lease-to-own solutions. This move may enable the company to better compete with cash advance competitor products like Chime MyPay and Dave ExtraCash, which both offer up to $500.

Higher APR-Focused

Higher-APR lender OppFi, saw originations grow +8% YoY, driven by consumer demand and credit model improvements allowing for higher average loan sizes. OppFi’s average yield of 130% was flat YoY.

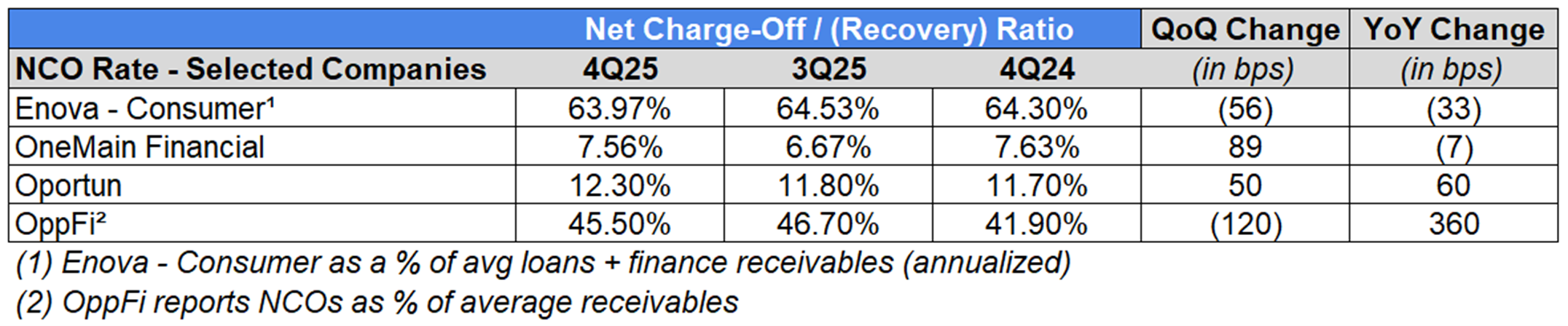

Enova (offers unsecured installment and lines of credit with APRs 34-200+% depending on state and product type), reported +2% YoY growth in consumer originations. Consumer origination growth has slowed due to Q2 credit tightening, following “minor elevated default metrics”.

Enova joined the charter wave, via its acquisition of Grasshopper Bank for $369Mn. Reportedly, Enova had been looking for a bank charter since at least 2020.

Second Look-Focused

Pagaya, a second-look lender, reported a +3% increase in network volume, driven by its personal loan segment which grew +10% YoY. Personal loans accounted for 65% of total network volume. Application volume from lending partners reached $263Bn, up from $197Bn a year prior, while the average conversion rate of applications remained at ~1%.

Credit Data

BNPL

While there has been much media concern surrounding BNPL usage and potential losses, underlying credit data has not shown substantial credit deterioration.

Klarna’s provision for credit losses rose +11bps YoY to 0.65% of GMV, but were (7)bps lower QoQ. The main driver of the higher provision for losses? Klarna’s push to grow its Fair Financing product. Klarna explained that it is required to book upfront provisions when growing its Fair Financing Portfolio.

Affirm’s delinquencies were slightly higher YoY, with its Monthly Installment Loan 30+ Day DQ Rate (Ex-Pay-in-4) for FY 2Q2026 at 2.7%, from 2.5% in FY 2Q2025. Management said that recent cohorts of monthly installment loans were tracking towards 3.5% NCOs (net charge-offs) as a % of cohort GMV.

Zip Co’s net bad debts (annualized net write-offs / opening receivables) as a % of GMV rose +7bps YoY to 1.73% for FY1H26.

Cash Advance

In Q4, cash advance apps Brigit and Dave both reported modest declines in credit performance while posting strong growth in originations. Despite the declines, the short-term nature of their products and their cash flow underwriting capabilities should help limit further deterioration in credit.

Brigit’s net advance loss rate rose +70bps YoY to 3.5%, which management attributed to expansion into new profitable user segments and the impact of a consumer that remains under pressure.

Dave’s 28-day delinquency rate rose to 2.19%, up +53bps YoY. However, its 28-day DQ rate declined (14)bps QoQ. Management said the increase was expected due to underwriting recalibration that was implemented alongside its new fee model to maximize gross profit.

Nonbanks

Enova, which lends at a higher APR and serves a clientele more prone to delinquency, reported an improvement in its NCO ratio, down (33)bps YoY. To note, Enova saw minor elevated default metrics in Q2 and tightened credit models for its consumer products.

OneMain Financial (7)bps reported a YoY improvement in its NCO ratio, helped in part by the reduction in the size of its “back book” (pre-Aug 2022 credit tightening).

Oportun reported a +60bps increase in its NCO ratio. However, NCOs came in at the low end of Q4 guidance after Oportun tightened credit in Q3 by reducing loan sizes and focusing on returning members.

OppFi which also lends at higher APRs and serves a clientele more prone to delinquency, reported a +360bps increase in its NCO ratio, due to higher delinquencies on its summer vintages.

Banks

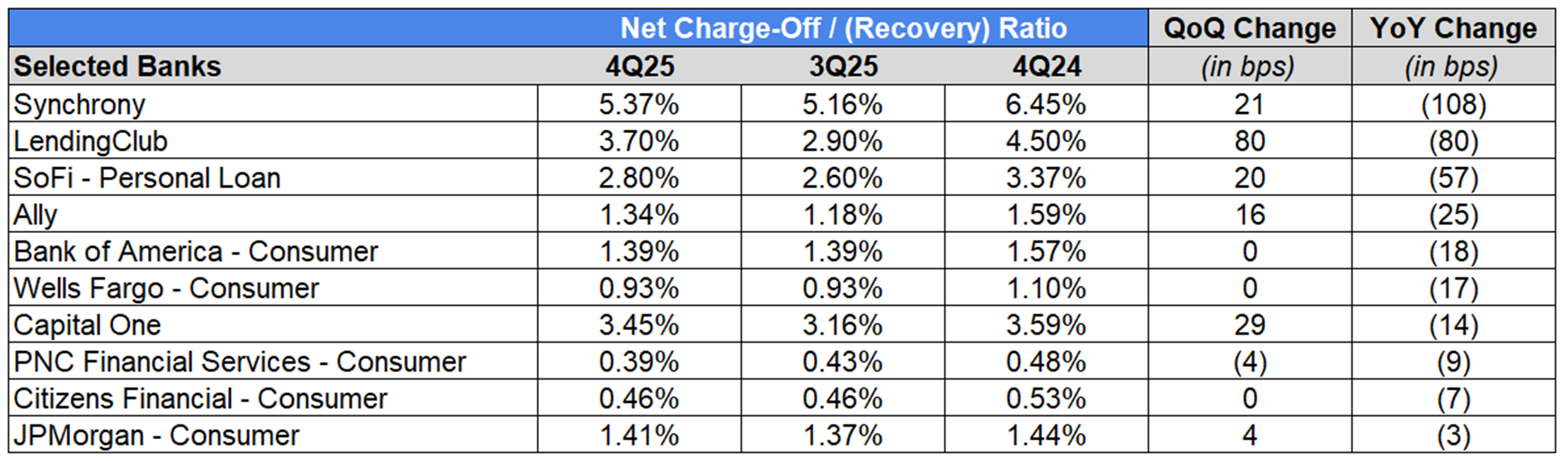

Turning to banks, Synchrony (108)bps, LendingClub (80)bps, SoFi – Personal Loan (57)bps, Ally (25)bps, Bank of America – Consumer (18)bps, Wells Fargo – Consumer (17)bps, Capital One (14)bps, PNC – Consumer (9)bps, Citizens – Consumer (7)bps, and JPMorgan – Consumer (3)bps all reported YoY improvements in their NCO ratios.

Synchrony attributed its improvement in NCO ratio to credit actions taken between mid-2023 and early 2024 and is now within its long-term target range of 5.5-6%.

LendingClub’s improvement in NCO ratio was driven by strong performance across all vintages. Its sequential increase was anticipated as more recent vintages mature.

SoFi’s NCO ratio improved but was affected by the sale of delinquent loans. Management disclosed that, accounting for the sale impact, it would estimate the NCO rate for personal loans to be 4.4%.

Capital One’s improvement in NCO ratio was led by its credit card portfolio, with its credit card NCO ratio down (111)bps YoY. Metrics were helped by the Discover acquisition, which has historically had lower losses and delinquencies than Capital One.

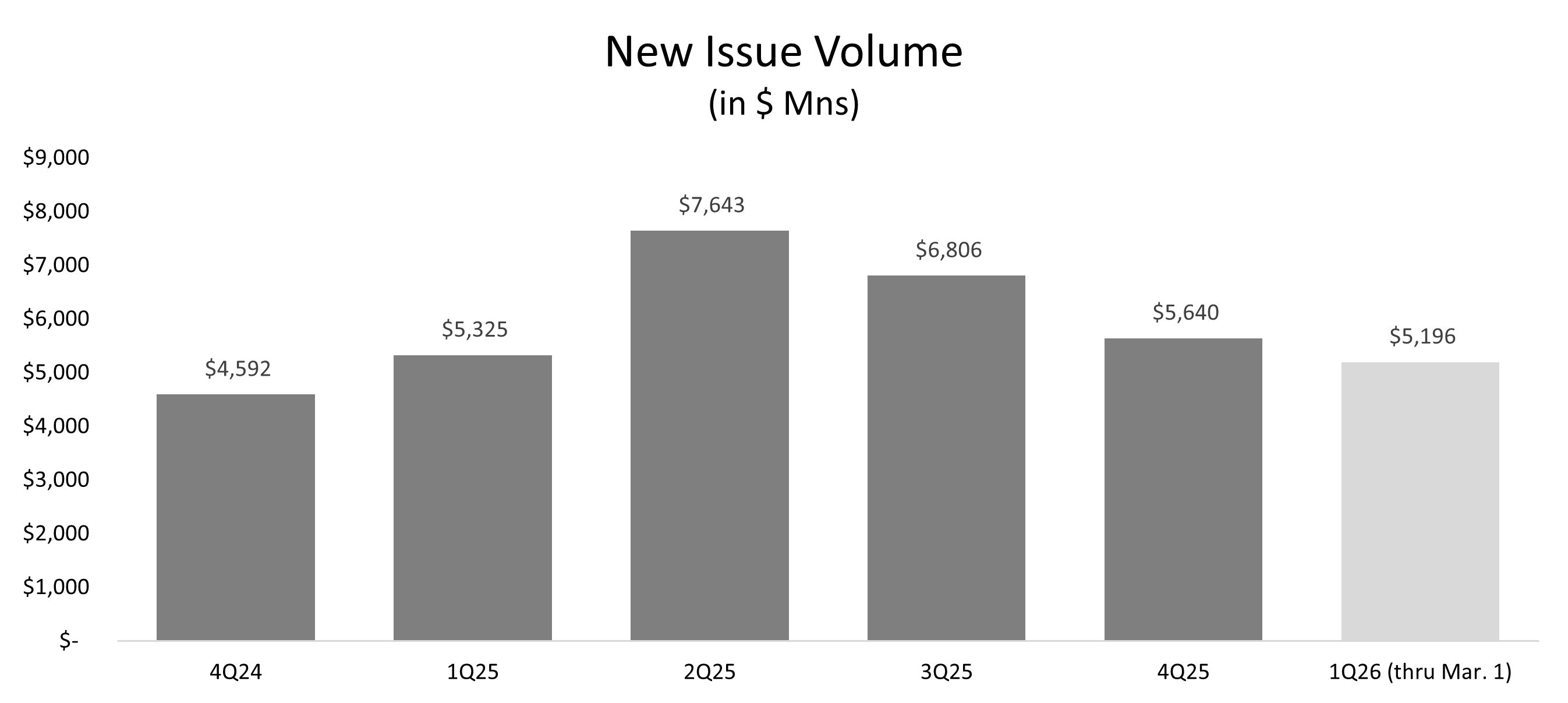

MPL New Issue Volume Growth Continued, but at a Slower Pace

In the fourth quarter, new issue volume for the consumer unsecured MPL market grew +22.8% higher on a YoY basis, but was (17.1)% lower on a QoQ basis. This made for slower YoY growth than Q3 (+63%) and Q2 (+96%). The YoY increase in new issue volume was driven by an increase in the number of deals (15 vs. 12) which outweighed a slight decline in average deal size, which was (1.7)% lower YoY at $376Mn.

2026 volumes are on pace to post substantial YoY growth. Through February, new issue volume was $5,196Mn, already nearing full 1Q25 levels ($5,325Mn).

Demand for these assets remains strong, and spreads continue to tighten. Affirm was able to drive a (104)bp decline in its cost of funds, on solid ABS execution and the repricing across all funding channels. In the quarter, Affirm priced its November static securitization at an all-in cost of funds of 5.96%, an over (100)bps improvement over its last static transaction which priced in 4Q24. Affirm said the deal was ~6x oversubscribed on robust investor demand, with the residual order book “particularly deep” and pricing at its lowest yield since Affirm began static securitizations.

Oportun reported that it had completed a $485Mn ABS transaction in February, its fourth consecutive issuance with a sub-6% funding cost and a AAA rating on its senior notes.

Pagaya CFO, Evangelos Perros, noted, “Last week, we closed an $800 million ABS deal that was oversubscribed even after upsizing from an initial size of $600 million.”

To go along with that, Pagaya President, Sanjiv Das, explained, “I'd like to reflect broadly on the capital markets environment, which remains very supportive for Pagaya. We see continued strong demand from across insurance funds along with traditional asset managers, while we are witnessing a higher level of rationality than we saw in 2025 from private credit. Overall, we would view the current environment as more of a steady state with healthy demand and execution, particularly for quality assets.”

Per the Finsight database, Pagaya - $1,694Mn, Affirm - $777Mn, Upstart - $480Mn, SoFi - $463Mn, Oportun - $441Mn, Upgrade - $427Mn, Mariner Finance - $375Mn, Lendmark - $360Mn, Regional Management - $253Mn, Achieve - $217Mn, and Americor - $153Mn were among the most active players in the fourth quarter.

Found value in our Q4 report? Subscribe here to receive our newsletter each Sunday.