Q3 2025 Review | Consumer Lending

.png)

Hi all, Cole here,

We come to you today with our quarterly consumer lending review. Catch up on the latest trends in the consumer lending space:

- takeaways from nonbank and bank earnings:

- originations (personal loan, BNPL, cash advance, high APR, second look, LTO)

- credit data (BNPL, cash advance, nonbank, bank)

- and an increase in MPL new issue volume

New here? Subscribe to receive our newsletter each Sunday.

Missed last quarter’s report? Catch up on key trends with my Q2 Consumer Lending Review.

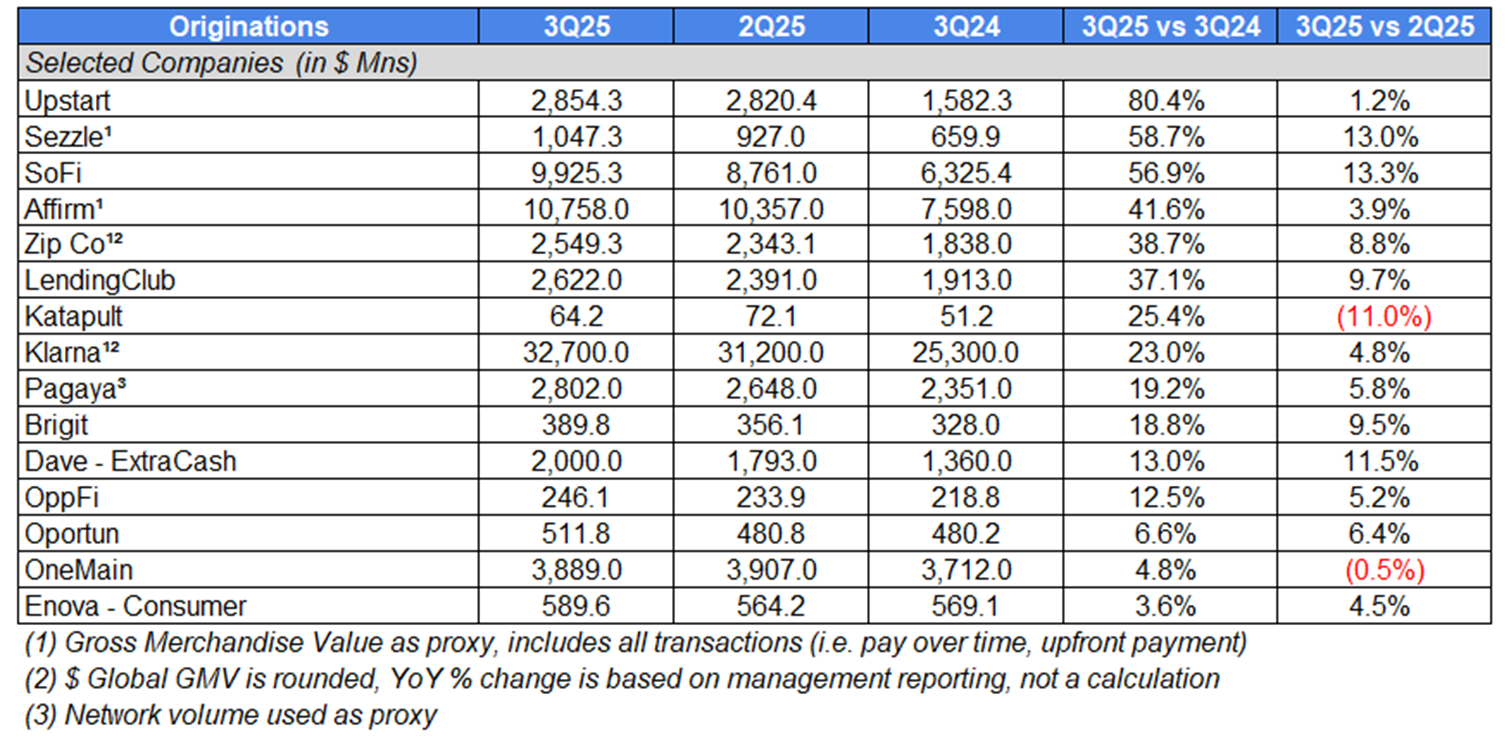

Consumer Loan Originations Post Robust Growth

Originations

In the third quarter, lenders continued to report strong YoY growth in originations across lending products (BNPL, cash advances, higher-APR (36%+ APR) loans, personal loans). YoY growth eased slightly from the second quarter, impacted by prior year comps, as originations did not start to pick up until the second half of 2024. Consumer demand for credit remains strong, with aggregate household debt hitting a record high of $18.59Tn in Q3, per New York Fed data.

Personal Loan-Focused

After a two-year period (mid-2022 to mid-2024) of declining or stagnant originations due to credit tightening efforts, unsecured personal loan volume continued to rebound.

In the third quarter, Upstart’s +80% origination growth was led by super prime (720+ credit score) originations, which were up +98% to $662Mn, representing 25% of all personal loan originations. Additionally, Upstart reported strong growth in its small-dollar originations, which were up +294% YoY to $138Mn and its auto originations which were up +357% YoY to $128Mn.

Consumer demand for Upstart loans continued to grow rapidly, with over 2Mn applications in Q3, up 30% QoQ. While a YoY increase in conversion rate to 20.6% helped originations, Upstart’s conversion rate was below the 23.9% reported in Q2. Management explained that its risk models responded to macro signals, modestly reducing approvals and increasing interest rates in the quarter. However, Upstart said it did not see any material deterioration in consumer credit strength.

SoFi reported strong origination growth, up +57% YoY, helped by “the introduction of interest-only periods for personal loans, new step-up repayment options for student loans, and home equity loans.” SoFi built upon its co-brand debit card business, which launched with Wyndham Hotels & Resorts in Q2, by partnering with Southwest Airlines to power its Rapid Rewards debit card.

In Q3, SoFi continued to invest in the crypto space. SoFi launched SoFi Pay, a crypto-powered global remittance product. SoFi Pay enables users to send money in local fiat abroad, “leveraging a layer 2 blockchain network and delivering local fiat into the account of the recipient”. Looking to 2026, SoFi plans to launch a SoFi USD stablecoin and integrate it into its SoFi Pay Wallet. And in November, SoFi launched SoFi Crypto, allowing users to buy, sell and hold crypto directly in its app.

LendingClub management attributed its +37% YoY origination growth to consumer demand, loan investor demand, and increased marketing efforts. 33% of originations were from its structured certificate program, under which LendingClub retains the senior note and sells the residuals, while 23% were extended seasoning held for investment, 23% were retained held for investment, and 21% were whole loan sales. Despite the growth in originations, LendingClub said that it remains very restrictive compared to pre-COVID credit standards. Looking ahead, LendingClub teased a potential rebrand expected in mid-2026.

Oportun reported a more modest but still solid +7% YoY growth in its originations as the lender took additional credit tightening actions such as lowering loan amounts and enacting hard declines. Oportun reported a substantial improvement in CAC as it focused on returning members, who made up 70% of originations in Q3, up from 64% in 1H25.

Oportun’s origination growth was led by success in its secured personal loan product, whose portfolio grew +58% YoY, reaching 8% of its owned portfolio balance. Oportun’s secured personal loans allow borrowers to secure their loans with their car titles, potentially allowing access to larger loans at lower rates than an unsecured loan. These loans have seen significantly better credit performance with the secured NCO rate ~500bps lower than the unsecured NCO rate through the first three quarters of 2025. Additionally, these loans generate 2x the revenue per loan compared to unsecured personal loans, primarily due to higher average loan sizes.

OneMain reported a +5% YoY increase in originations, even as the company maintains tighter credit standards and higher pricing. OneMain has offered smaller initial loan amounts to certain customers, with the goal of expanding its eligible customer base without taking on additional risk. In March, OneMain filed an application with the Utah Department of Financial Institutions and the FDIC to form OneMain Bank (an industrial loan company). The status of the application is still pending.

Management noted that origination growth was helped by the creation of a loan origination channel through its credit card business. OneMain has continued to gain traction with its BrightWay credit cards, growing receivables +52% YoY to $834Mn.

BNPL-Focused

BNPL rolls on, driven by increased market penetration and increased usage by consumers.

Sezzle’s +59% YoY growth in GMV (gross merchandise volume) led BNPL players, with its growth driven by greater usage of subscription products and increased consumer engagement. Sezzle marketing efforts emphasized its subscription product over On-Demand in Q3, leading to a +17% increase in active subscribers QoQ, compared to a (18)% QoQ decline in Monthly On-Demand users. The increase came even as the company increased pricing on its subscription products from $1 to $2 per month. Quarterly purchase frequency rose to 6.5x, up from 5.4x a year prior.

Notably, Sezzle Anywhere subscribers are power users of the product, and averaged 10 more orders than non-subscribers in Q3. Further, the top 10% of Sezzle’s Anywhere subscribers used the product an average of 36x in the past 90 days.

Sezzle is the latest fintech to explore a bank charter. Management disclosed that it has hired consultants and attorneys to look into applying for an ILC (industrial loan company) charter. Sezzle explained that if it decides to apply, it plans to do so in the first half of 2026. Currently, Sezzle partners with WebBank to offer its financial products.

Affirm’s YoY GMV growth of +42% also benefited from a more engaged user, with transactions per active consumer of 6.1x, up from 5.1x a year prior. At the same time, its average order value declined (7)% YoY to $260, in-line with strategy. GMV growth was led by 0% APR products, with its 0% APR Monthly products +74% YoY and Short-Term 0% APR +50% YoY. Its interest-bearing product grew +35% YoY.

The Affirm Card continues to scale, with 2.8Mn active cardholders at quarter end, up +101% YoY and card GMV of $1,427Mn, up +135% YoY. Specifically, in-store usage of the Affirm Card grew +170% YoY. In-store usage is a positive sign for Affirm’s strategy, which is to capture a greater share of consumer payments, including for routine purchases.

Zip Co, a BNPL provider that operates in the U.S., Australia, and New Zealand, reported a +39% increase in volumes. For context, roughly three-quarters of its volumes come from the U.S. market, which grew +51% YoY. In August, Zip integrated with autofill on Google Chrome, allowing customers to use Zip without switching apps or re-entering payment details.

Klarna reported +23% YoY GMV growth YoY, helped by a +43% increase in U.S. GMV and +73% increase in Southern Europe GMV. Klarna’s most mature market, Sweden, posted solid +18% YoY GMV growth.

Klarna’s Fair Financing (typically a 6-12 month term product which may charge interest) volumes soared, up +244% YoY. Klarna added 25k merchants to Fair Financing in Q3, bringing the total to 151k. Klarna said its Fair Financing offering has a transaction margin over 2x the group average.

The Klarna Card accounted for over 15% of total transactions, up from 10% in Q2. Klarna Card has gained early traction, recording 4Mn signups since its July launch.

Cash Advance-Focused

Consumers looking for a way to bridge the gap between paychecks have increasingly turned to earned wage access and short-term cash advance products.

Brigit has reported strong growth since being acquired by Upbound Group, with volumes growing +19% YoY. Brigit grew its average revenue per user +11% YoY to $13.74 on higher expedited transfer fees, deeper engagement with marketplace offers, and a continued shift toward the Premium tier.

Brigit’s line of credit product is now in beta testing. The product offers a loan size up to $500, twice the cap on its Instant Cash advances. Management aims for the product to bridge the gap between smaller ticket BNPL and larger ticket lease-to-own solutions. This move may enable the company to better compete with cash advance competitor products like Chime MyPay and Dave ExtraCash, which both offer up to $500.

Dave is also exploring new product offerings. The cash advance player is working to add a BNPL product, which is currently in internal testing with a handful of employees. Dave expects to have customers start testing the product in Q1. More than half of Dave members engage in some form of BNPL transaction and Dave has access to significant member cash flow and underwriting data. With the move into BNPL, Dave will be entering a market dominated by mature players such as Affirm, Afterpay, Klarna and PayPal.

Dave reported a +49% YoY increase in originations, driven both by the size of originations (+20% YoY to $207) and by growth in monthly transacting members (+17% YoY to 2.8Mn). At the same time, Dave has continued to grow its average revenue per ExtraCash advance, which grew +36% YoY to $13. Dave attributed the increase to expanded approval limits under a new fee model, enhancements from CashAI, and the increasing tenure of its member base.

Higher APR-Focused

Higher-APR lender OppFi, saw originations grow +12% YoY, driven by consumer demand and credit model improvements allowing for higher average loan sizes. OppFi’s average yield of 133% represented a marginal decline from 134% a year prior.

Enova (offers unsecured installment and lines of credit with APRs 34-200+% depending on state and product type), reported +4% YoY growth in consumer originations. Consumer origination growth has slowed due to Q2 credit tightening, following “minor elevated default metrics”.

Second Look-Focused

Pagaya, a second-look lender, reported a +19% increase in network volume, driven by its personal loan segment which grew +31% YoY. Personal loans accounted for 64% of total network volume. At the same time, its combined point-of-sale (“POS”) and auto volumes reached 32% of total volumes, up from just 9% a year prior. Application volume from lending partners reached $266Bn, up from $203Bn a year prior, while the average conversion rate of applications remained at ~1%.

Lease-to-Own-Focused

For those who are unfamiliar, Katapult provides lease-to-own solutions to nonprime consumers. Lease-to-own (“LTO”) offers an alternative to BNPL and credit products, allowing customers to make payments towards owning a product. Customers can make payments to lease, buy out the plan or return the product at any time. On average, Katapult’s typical lease is for about $700.

Katapult grew gross originations +25% YoY, with 55% of originations from repeat customers. Katapult launched Apple in its Katapult app marketplace. In the marketplace, consumers can pay via Kpay (a 1-time use virtual card) or be redirected to merchant-partner sites.

Credit Data

BNPL

While there has been much media concern surrounding BNPL usage and potential losses, underlying credit data continues to hold up.

While Klarna’s provision for credit losses rose +28bps YoY to 0.72% of GMV, its realized losses decreased (1)bp YoY to 0.44% of GMV. A main driver of the higher provision for losses? Klarna’s push to grow its Fair Financing product. Klarna explained that it is required to book upfront provisions when growing its Fair Financing Portfolio.

Affirm’s delinquencies were flat YoY, with its Monthly Installment Loan 30+ Day DQ Rate (Ex-Pay-in-4) for FY 1Q2026 at 2.8%, in-line with FY 1Q2025 but above the 2.3% reported in 4Q2025. Management said that recent cohorts of monthly installment loans were tracking towards 3.5% NCOs (net charge-offs) as a % of cohort GMV.

Zip Co’s net bad debts (annualized net write-offs / opening receivables) as a % of GMV rose +6bps YoY to 1.65%.

Cash Advance

In Q3, cash advance apps Brigit and Dave both reported modest declines in credit performance while posting strong growth in originations. Despite the declines, the short-term nature of their products and their cash flow underwriting capabilities should help limit further deterioration in credit.

Brigit’s net advance loss rate rose +30bps YoY to 3.3%, which management attributed to testing into new marketing channels and custom segments.

Dave’s 28-day delinquency rate rose to 2.33%, up +55bps YoY. However, its 28-day DQ rate was lower than the 2.40% in Q2 and its September 28-day DQ rate was 2.19%, suggesting a positive trend.

Nonbanks

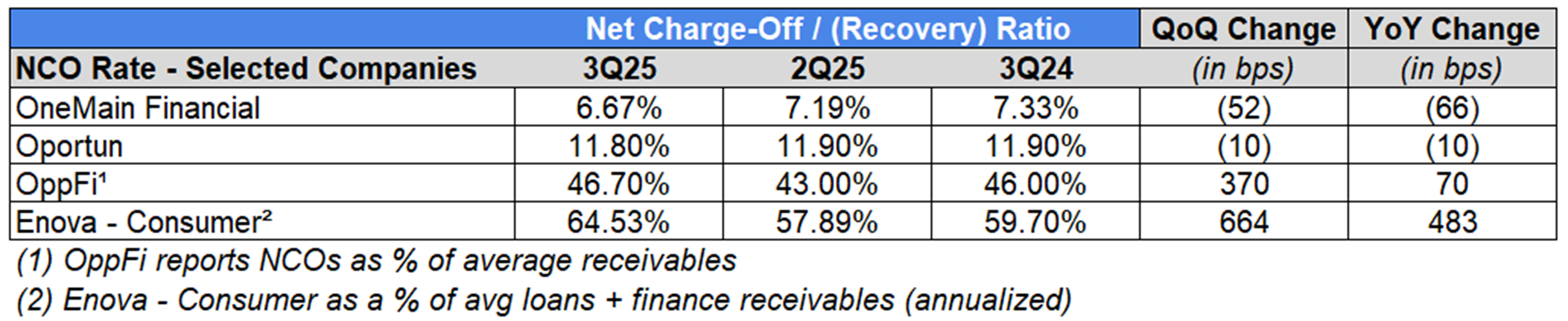

OneMain Financial (66)bps reported a YoY improvement in its NCO ratio, helped in part by the reduction in the size of its “back book” (pre-Aug 2022 credit tightening).

Oportun reported a (10)bps improvement in its NCO ratio. Oportun expects a rise in its NCO ratio in Q4, and tightened credit in Q3 in response to the 30+ day DQ rate coming in at the high end of expectations. It has taken loan sizes down (unsecured down (5)% YoY and secured down (7)% YoY) to tighten credit.

OppFi and Enova, which lend at higher APRs and serve a clientele more prone to delinquency, reported increases in NCO ratios. OppFi reported a +70bps YoY increase in its NCO ratio, due to elevated charge-offs from early summer vintages offsetting higher recoveries of previously charged off loans. Subprime lender Enova reported a +483bps rise in consumer NCOs. As mentioned in the prior section, Enova saw minor elevated default metrics in Q2 and tightened credit models for its consumer products. With the tightening, management says that credit performance has returned to normal and now exceeds expectations.

Banks

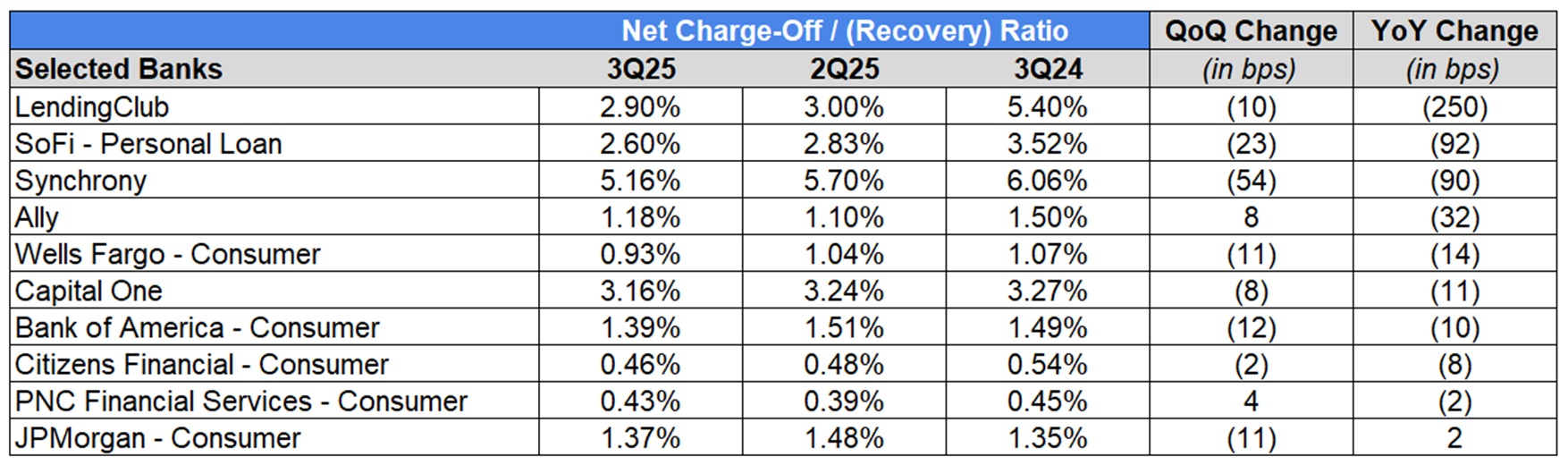

Turning to banks, LendingClub (250)bps, SoFi – Personal Loan (92)bps, Synchrony (90)bps, Ally (32)bps, Wells Fargo – Consumer (14)bps, Capital One (11)bps, Bank of America – Consumer (10)bps, Citizens – Consumer (8)bps, and PNC – Consumer (2)bps all reported YoY improvements in their NCO ratios. JPMorgan reported a nominal increase of +2bps in its NCO ratio YoY.

LendingClub’s improvement in NCO ratio was driven by recent vintages added to its balance sheet. CEO Scott Sanborn noted that the lender remains very restrictive compared to the pre-COVID era, especially in the lower credit area.

SoFi’s NCO ratio improved, but was affected by the sale of delinquent loans. Management disclosed that, accounting for the sale impact, it would estimate the NCO rate for personal loans to be 4.2%, still below the 4.5% it estimated in Q2.

Synchrony attributed its improvement in NCO ratio to credit actions taken between mid-2023 and early 2024. CEO Brian Doubles said that credit actions have outperformed expectations and that Synchrony has begun to gradually reverse some tightening in areas it sees strong risk-adjusted growth opportunities.

Capital One’s improvement in NCO ratio was led by its credit card portfolio, with its credit card NCO ratio down (99)bps YoY. Metrics were helped by the Discover acquisition, which has historically had lower losses and delinquencies than Capital One.

Despite the YoY improvement, a number of bank consumer divisions’ net charge-off ratios have risen above pre-pandemic (3Q19) levels, with Capital One +78 bps, Ally +35 bps, JPMorgan – Consumer +21 bps, and Bank of America - Consumer +21 bps.

Due to recent credit improvements, Synchrony’s NCO ratio dropped below pre-pandemic (3Q19) levels by (91) bps (after previously breaching such levels). Additionally, Citizens – Consumer came in below pre-pandemic (3Q19) levels by (7)bps.

PNC’s NCO ratio came in (19) bps lower than pre-pandemic (3Q19) levels but the bank has grown home equity + residential real estate loans as a % of its consumer loan book from pre-pandemic levels. Looking at broader industry data, these types of loans have carried lower delinquency rates than credit card and auto loans and likely translate into lower net charge-offs.

Dollar NCOs (Banks and Nonbanks)

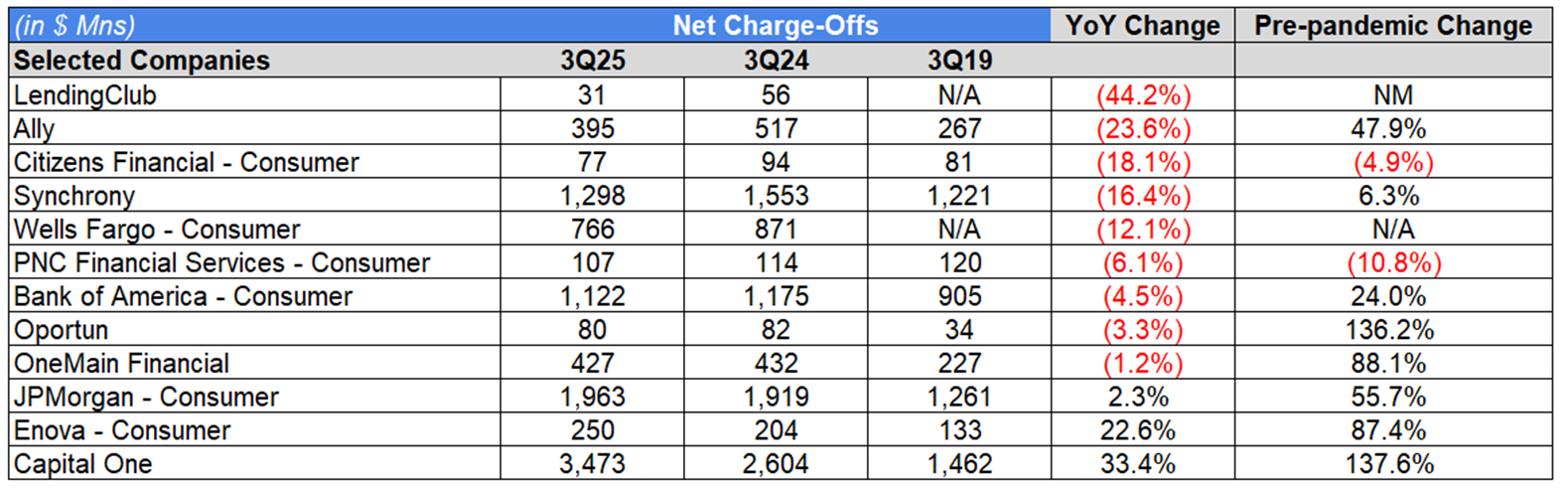

Declines in net-charge offs (in $ values) were reported by LendingClub (44.2)%, Ally (23.6)%, Citizens – Consumer (18.1)%, Synchrony (16.4)%, Wells Fargo – Consumer (12.1)%, PNC – Consumer (6.1)%, Bank of America – Consumer (4.5)%, Oportun (3.3)%, and OneMain Financial (1.2)% on a YoY basis.

Increases in net-charge offs (in $ values) were reported by Capital One +33.4%, Enova – Consumer +22.6%, and JPMorgan – Consumer +2.3%. Capital One YoY increases were affected by its acquisition of Discover.

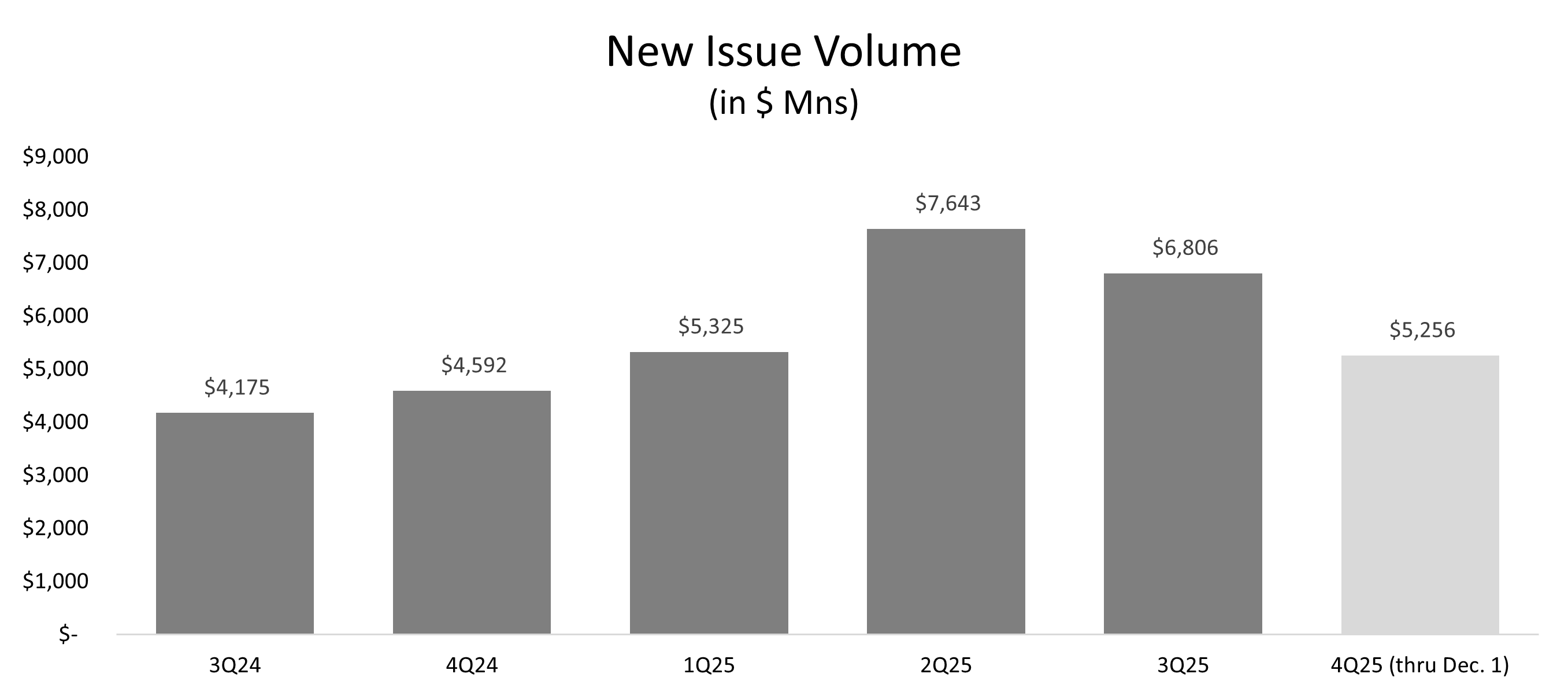

MPL New Issue Volume Continues to Grow

In the third quarter, new issue volume for the consumer unsecured MPL market jumped +63.0% higher on a YoY basis, but was (11.0)% lower on a QoQ basis. The YoY increase in new issue volume was driven by an increase in the number of deals (16 vs. 11) and by an increase in average deal size, which grew +12.1% YoY to $425Mn.

2025 volumes have continued to grow with cumulative new issue volume through November of $25,030Mn outpacing 2024 levels by 50.6%. 4Q25 new issue volumes of $5,256Mn (through November) have already eclipsed full quarter volume from 4Q24 (of $4,592Mn).

Demand for these assets remains strong, and spreads continue to tighten. Upstart CEO David Girouard noted, “In September, we also issued a securitization with strong demand, leading to significant oversubscription of all classes despite upsizing and tightening of spreads. This ABS deal involved 30 investors, including 7 first-timers, demonstrating the strength of Upstart's reputation in the market.”

Affirm was able to drive a (98)bp decline in its cost of funds, on solid ABS execution and the repricing of ABS and warehouse facilities. In the quarter, Affirm closed an ABS deal for $1.1Bn at its lowest weighted-average yield since FY2022. COO Michael Linford commented, “I mean the capital markets probably continue to be very constructive for our asset. I think there was a lot of activity in the ABS market over the past 3 or 4 months, and we were really pleased with just the engagement that so many of our investors gave us and the flight to quality that we're seeing.”

During the quarter, Oportun issued $538Mn in ABS notes at a 5.29% weighted average yield, its lowest cost ABS issuance since October 2021. Oportun CFO Paul Appleton explained, “Cost of debt was lower sequentially, decreasing from 8.6% in the second quarter to 8.1% in the third quarter, closely aligning with our 8% unit economics target. This improvement reflects the positive impact of recent lower cost ABS issuance, the refinancing of higher cost ABS debt as well as the repayment of corporate debt.”

Pagaya CEO Gal Krubiner provided color on capital markets, saying, “Demand for our assets remains consistent and robust” and explaining, “I think that putting the Liberation Day a little bit of like volatility aside, this year, demand for the different parts of the capital structure is very robust. So when we look on the senior -- the spread of the senior capital stack, it's actually been fairly steady throughout the year. And on the junior pieces actually came a little bit even tighter, something like 50 basis points, call it, January, February versus now.”

Per the Finsight database, Pagaya - $1,410Mn, Affirm - $1,100Mn, Oportun - $538Mn, Bankers Healthcare Group - $500Mn, SoFi - $466Mn, Upstart - $435Mn, Reach Financial - $424Mn, Lendmark - $400Mn, Republic Financial - $375Mn, Best Egg - $338Mn, Upgrade - $317Mn, Woodward Capital Management - $303Mn and Sunbit - $200Mn were among the most active players in the third quarter.

Found value in our Q3 report? Subscribe here to receive our newsletter each Sunday.