FOMC Minutes; FDIC Tweaks Signage Rule; Klarna Inks Loan Sale Deal

.png)

FOMC minutes show divided policymakers. FDIC proposes digital signage rule tweaks. CFPB may rollback remittance provider oversight. FHFA director opens new line of attack on Fed. CFPB drops investigation of Credova. Bullish takes IPO proceeds in stablecoins. Klarna inks loan sale deal with Nelnet.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

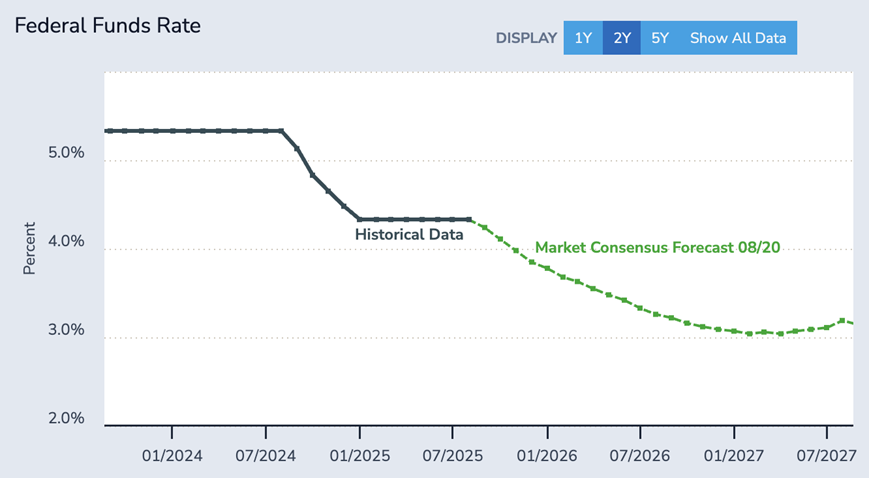

FOMC Minutes Show Policymakers Divided

Minutes of the most recent Federal Open Market Committee meeting show policymakers are divided on whether or not to cut rates. The FOMC must weigh what appears to be an increasingly softening labor market against stubbornly persistent inflation, which, many fear, will be exacerbated due to the impact of tariff policy.

Minutes of the meeting note that “participants generally pointed to risks to both sides of the Committee’s dual mandate, emphasizing upside risk to inflation and downside risk to employment.” Per the meeting minutes, “a majority of participants judged the upside risk to inflation as the greater of these two risks,” although some FOMC members saw “downside risk to employment the more salient risk.” Fed Governors Waller and Bowman voted against the decision to keep rates where they are, which is the first time in more than 30 years that multiple FOMC members voted against the consensus position.

FDIC Proposes Tweaks to Digital Signage Rule

The FDIC is proposing tweaking digital signage rules to accommodate what banks have said are practical difficulties in implementing the regulations as written. The rules were finalized in December 2023 and largely formalized existing, long-standing guidance. The intention of the signage requirement is to help consumers distinguish between FDIC-insured banks and their insured deposit products vs. non-insured products or entities, like third-party fintechs that partner with banks. Some industry stakeholders have complained that the rule is overly prescriptive and argued that banks would benefit from more flexibility in how they implement the requirement, particularly on web pages and mobile devices, where space is limited. Some also raised concerns about consumer confusion when users are on third-party non-bank sites that list both insured and uninsured products. Last week’s proposal would remove the requirement that banks inform customers of FDIC insurance on a bank’s landing page and would allow banks to include the FDIC disclaimer on fewer pages.

CFPB May Rollback Oversight of Remittance Providers

The Consumer Financial Protection Bureau is mulling a change that could reduce oversight of companies in the cross-border payments and remittance space. Specifically, the CFPB said earlier this month that it is considering changing the definition of a “larger” participant in this market. Presently, the larger participant threshold is defined as nonbank firms that make more than one million international transfers annually.

The CFPB has said it is concerned that this definition may cause burdensome costs and unnecessary regulatory oversight. According to a post the CFPB made on the matter, “The Bureau is concerned that the benefits of the current threshold may not justify the compliance burdens for many of the entities that are currently considered larger participants in this market, and that the current threshold may be diverting limited Bureau resources to determine whom among the universe of providers may be subject to the Bureau’s supervisory authority and whether these providers should be examined in a particular year.”

CFPB Drops Investigation of “Shoot Now, Pay Later” Company

The Consumer Financial Protection Bureau has dropped an investigation into a firearm-focused buy now, pay later provider. The firm in question, Credova, was acquired by PSQ Holdings, where Donald Trump Jr. serves on the board, in March 2024. PSQ also operates a payments firm and a marketplace that the company describes as aligned with “traditional American values.” The CFPB sent PSQ Holdings a letter, signed by chief legal officer Mark Paoletta, that it was closing the investigation. The letter said in part, “After reviewing the case, the Bureau has determined that this investigation exemplifies the type of weaponization against disfavored industries and individuals that President Trump and Acting Director Vought are committed to ending. Credova’s use of innovative financial technology solutions to provide consumer financing to facilitate Americans exercising their Second Amendment rights made it a target for the Bureau.”

Bullish Takes IPO Proceeds in Stablecoins

Crypto exchange Bullish raised $1.15Bn in its IPO, and, in an interesting twist, took the proceeds it raised via stablecoins. The company sold shares at $37 a pop, and, once trading began, saw its share price rise as high as $118. But the real news may be that the company took the proceeds from its IPO in the form of stablecoins, primarily in Circle’s USDC on the Solana blockchain and Ripple’s RLUSD on XRP Ledger. Bullish CFO David Bonanno commented on the decision, saying, “We view stablecoins as one of the most transformative and widespread use cases for digital assets. Internally, we leverage them for rapid and secure global fund transfers, especially on the Solana network. We believe our collaborations with the stablecoin issuers represented here, including their listings on our Bullish exchange, demonstrate how the infrastructure and liquidity we’ve built at Bullish helps power their businesses.”

Klarna Inks Loan Sales Deal with Nelnet

Swedish buy now, pay later giant Klarna is planning to sell up to $26Bn in loans to Nelnet in advance of its renewed attempt to IPO. Nelnet has agreed to buy newly originated pay-in-four receivables on an ongoing basis. The commitment from Nelnet gives Klarna greater flexibility in how it manages its balance sheet. Niclas Neglén, Klarna’s CFO, commented on the deal in a press release, saying, “This is a landmark transaction for Klarna in the U.S. Our partnership with Nelnet allows us to scale a core product responsibly, while continuing to deliver smooth, interest-free payment experiences to millions of consumers.” Klarna was on track to IPO earlier this year, before President Trump’s “Liberation Day” tariff announcements sent markets swooning. A number of firms that had planned public offerings, including Klarna, chose to delay doing so. But since then, markets have steadied and recent fintech and crypto IPOs have been generally well received by the market. Klarna is reportedly resuming plans for its public offering, though a specific date isn’t yet publicly known.