PCE Price Index Climbs; Banks Pass “Stress Tests”; Circle and Nomura Partner

.png)

The core PCE price index rose at a 3.4% annualized rate in May. Banks pass their stress tests. More consumers complain of bank account closures. Housing bill tweaks brokered deposit rules. Amex forks over $700Mn for TheFork. Adyen acquires billing platform Orb. Major banks push back on BNPL. Circle and Nomura partner on forex.

Before entering the card space, fintechs and brands must understand how BIN sponsorship works, who bears regulatory responsibility, and why the choice of issuing bank can determine whether a program scales or breaks. Our VP of Card Products, Juan Wiley, breaks it down in his new Insights piece so that fintechs and brands can approach their card programs with clarity.

New here? Subscribe to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

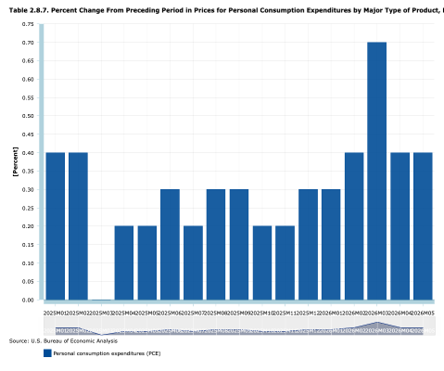

PCE at 3.4%, “Stress Test” Results

The personal consumption expenditure price index rose at a 3.4% annual rate in May, excluding food and energy, the Commerce Department’s report showed last week. Including food and energy, the PCE index showed inflation hitting a seasonally-adjusted 4.1% annual rate, making it the highest rate of inflation using the PCE metric since April 2023. Meanwhile, GDP came in at a seasonally-adjusted 2.1% on an annualized basis, handily exceeding the consensus forecast of 1.7%.

The 32 banks that underwent “stress tests” collectively demonstrated strong performance on the annual assessment. In the exam’s most extreme scenario, the group, as a whole, would see a drop in common equity Tier 1 capital ratio of 1.6%. No individual bank came within 2 percentage points of the minimum ratio of 4.5%. The banks’ capital requirements will remain unchanged, as the Fed is debating reforms to its stress testing process.

More Consumers Complain of Bank Account Closures

There has been a surge in consumer back account closures in recent months, driving impacted account holders to file complaints with the Consumer Financial Protection Bureau, according to new analysis from McCarthy Hatch. The data, reported in American Banker, show more than 20,000 consumers filed complaints about the abrupt closure of an account from December 2025 to May 2026. The new data point comes amidst a number of Executive Orders from the Trump administration that could discourage financial institutions from serving immigrants. One E.O. specifically flagged the use of ITINs, or individual tax ID numbers, as a potential risk. People who do not qualify for a Social Security number can apply for an ITIN from the IRS in order to make legally required income and payroll tax payments. Interestingly, per the McCarthy Hatch data set, Block was the most complained about when it came to account closures by an order of magnitude. More than 4,100 consumers complained about Block during the December to May period, while the second-most complained about firm, Capital One, saw just 1,615 complaints during the same period. Jim McCarthy, the chairman of the firm the analyzed the complaint data, told American Banker, “The big takeaway is that consumers are screaming for help in plain English: 'My account was suddenly closed,' 'The bank would not tell me why,' and 'I could not access my funds.”

Housing Bill Tweaks Brokered Deposit Rules

The 21st Century ROAD to Housing Act has passed both the House and the Senate, though it remains unclear when (or if) President Trump will sign the bill. While, as the name suggests, the measure primarily addresses the housing market, there are a couple of provisions that, if enacted, could have significant impacts on banks and fintechs. Specifically, two measures related to brokered deposits, which, supporters argue, would enable banks to free up capital by excluding certain kinds of deposits from the definition of brokered. Under the new law, reciprocal deposits, like those facilitated by networks like IntraFi, and custodial deposits, a common structure used in bank-fintech partnerships, would generally not be treated as “brokered” for depositories with less than $10Bn in assets and comprised less than 20% of a bank’s deposit base. The changes are tangentially related to housing: the incrementally available capital could be used to increase consumer mortgage lending, advocates of the change said.

Amex Pays $700Mn for TheFork

American Express is paying up to acquire restaurant reservation management system TheFork. The card company will pay Tripadvisor $700Mn, according to the deal announcement last week. The acquisition of TheFork will complement American Express’ acquisition of dining platforms Resy and Tock. The three combined boast a network of more than 75,000 restaurants, American Express’ news release says. Rafa Marquez, President of International Card Services at American Express commented on the acquisition of TheFork, saying, “Dining is one of the most important ways people engage with our brand. Over time, the proposed acquisition would help us enrich our differentiated Membership Model by offering Card Members more ways to discover, book and access great restaurants, while helping our partners reach more diners and grow their businesses.”

Adyen Acquiring Billing Platform

Payment processor Adyen is acquiring billing and payments platform Orb, the companies announced earlier this month. The all-cash deal is worth $335Mn, according to the news release. SF-headquartered Orb had raised a total of $44Mn in funding. Orb’s platform takes a “technology-first” approach to billing and invoicing, with a focus on high-growth digital businesses. Orb’s billing and invoicing capabilities logically complement Adyen’s core focus on payments processing. Adyen co-CEO Ingo Uytdehaage commented on the acquisition, saying, “Our customers increasingly need infrastructure that can handle complex, high-volume usage models, particularly as AI reshapes how software is priced and consumed. The structural complexity of modern billing has become the kind of infrastructure problem Adyen is built to take on.”

Major Banks Push Back on BNPL

Money center banks are continuing to push back on encroachments from buy now, pay later players. Companies like Klarna and Affirm have expanded to offer banking-like products, with both firms offering debit cards that consumers can use to make both “pay now” and “pay later” transactions. Both also offer savings accounts through bank partnerships. But major banks have slowly but surely been evolving their offerings to fight back. Per Banking Dive, four out of five of the country’s largest banks now offer some flavor of installment lending plan tied to their debit cards. And, earlier this month, Bank of America launched a new, longer-term flexible payment option that enables users to finance purchases for between three and 18 months by paying a flat monthly fee, rather than an interest charge.

Circle and Nomura Partner on Forex

USDC-issuer Circle and Japanese bank Nomura are partnering on a cross-border foreign exchange settlement initiative that could launch in early 2027. The relationship will enable Japanese businesses to trade yen for USDC, according to reports from Coindesk and Nikkei. Per BIS data, Japan’s forex market sees about $440Bn in transaction volume daily. Typical wire transfers can take multiple days to clear and settle, resulting in idle capital. Processing such transactions via stablecoins and blockchain can be near-instant, resulting in significant capital efficiencies at scale. The partnership was made possible thanks to a recent change to Japanese law, allowing dollar-denominated stablecoins to be used locally by Japanese corporates.

In other Japan-crypto news, Ripple’s RLUSD stablecoin has officially gone live in the country, after winning regulatory approval to do so. The Japan Financial Services Agency OK’d RLUSD as an electronic payment instrument as defined by the country’s Payment Services Act. Japan is generally considered one of the most highly regulated financial services markets in Asia. RLUSD will be available to both institutional and retail customers via a partnership with Japanese digital asset firm SBI VC Trade.