Fed Gov Vows to Fight; CFPB Files Suit Against Synapse; Elavon Offers Rev-Based Loans

.png)

Fed Gov Lisa Cook vows to fight firing. More borrowers are taking longer-term auto loans. CFPB looks to narrow non-bank supervision, files complaint against bankrupt Synapse. Anchorage Digital resolves OCC consent order. Is Klarna’s IPO back on? Fifth Third acquires DTS Connex. Thread selects Fiserv’s Finxact. U.S. Bank’s Elavon to offer rev-based financing.

Cross River and Sightline Payments announced the launch of Sightline Debit this week, a groundbreaking solution designed to streamline gaming transactions, reduce operator costs, and give customers more control — all with funds in FDIC insured accounts. Read the full press release here.

Keep an eye on your inboxes. Next week we will send out our Q2 Consumer Lending Review.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

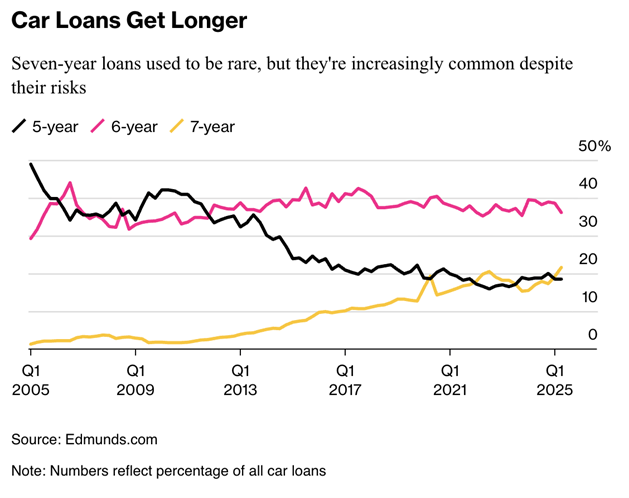

One in Five Auto Loans Carries A 7-Year Term Now

Federal Reserve Governor Lisa Cook vowed to fight President Trump’s move to oust her from her role on the Federal Reserve Board. Trump’s effort centers around allegations that Cook committed mortgage fraud by claiming two separate properties as her “primary” residence on loan documents. The Federal House Finance Agency Director, Bill Pulte, made a criminal referral to the Department of Justice in the matter, though the DOJ has not filed any charges. Federal Reserve governors can only be removed “for cause,” but, as no one in the role has ever been removed before, the definition of “for cause” remains murky. Removing Cook, whose term was not set to expire until 2038, would give Trump the opportunity to secure a four-person majority of the Fed’s seven-person board. Market reaction was fairly muted, though yields on 30-year bonds rose, suggesting investors believe inflation pressure could increase if Trump is successful at replacing Cook with a more dovish policymaker.

In other news, vehicles have become so expensive that longer-term financing is becoming increasingly common. More than one in five auto loans in 2Q25 carried a term of seven years. Longer-term loans carry a variety of downsides for borrowers, including, of course, greater interest expense over the life of the loan: average interest paid on an 84-month auto loan amounts to $15,460. Because of how quickly vehicles typically depreciate, owners can also more easily end up with negative equity, meaning if they want to trade in or sell the vehicle, it’s worth less than the outstanding principal on the loan.

CFPB Looks to Narrow Non-Bank Supervision, Files Complaint Against Synapse

The Consumer Financial Protection Bureau is proposing a rule that would limit its ability to supervise non-bank entities. The rule would seek to define a standard of “risks to consumers with regard to the offering or provision of consumer financial products or services,” which would limit the entities the Bureau could designate as falling under its jurisdiction. The impacts could be far reaching, with the proposal noting that “the Bureau expects that under the proposed rule it will be less likely to designate any particular entity for supervision, all other factors being equal.” Comments will be accepted on the proposed rule until September 25th.

In other Bureau news, the CFPB simultaneously filed a complaint and a stipulated judgment and final order in the Synapse debacle. The complaint alleges that Synapse “violated the Consumer Financial Protection Act of 2010 by failing to maintain adequate records of the location of consumers’ funds and failing to ensure those records matched the records maintained by its partnering banks, causing consumers to lose access to their funds.” The Chapter 11 Trustee for the Synapse estate, former FDIC Chair Jelena McWilliams, agreed to a settlement with the CFPB, which includes a $1 civil money penalty. The inclusion of that penalty opens up the possibility the CFPB can use its civil penalty fund to pay compensation to end users who did receive all of their funds back after Synapse collapsed last April.

Anchorage Resolves OCC Consent Order

The OCC has lifted a consent order against Anchorage Digital, the only crypto firm to hold a national bank charter. The order stemmed from issues in the national trust bank’s anti-money laundering compliance program. The order found that Anchorage had inadequate controls and procedures for customer due diligence and suspicious activity monitoring. Anchorage Digital cofounder and CEO published a letter following the resolution of the consent order, which read in part, “With our consent order lifted, we’ve proven definitively that crypto and federal oversight are not mutually exclusive — and can in fact be stronger working in tandem.”

Is Klarna’s IPO Back On?

Buy now, pay later giant Klarna’s IPO may be back on. The company, once valued at more than $45Bn, will seek a valuation of around $14Bn next month, Reuters is reporting. Klarna had previously intended to IPO this April, but put plans on hold amid the market tumult following the announcement of President Trump’s “Liberation Day” tariffs. Klarna is targeting a per share price of between $34 and $36, which would raise about $1Bn in new funding, according to the report.

In other Klarna-related news, the company has inked a deal for a €1.4Bn (about USD $1.6Bn) structured finance facility with Spanish bank Santander. The warehouse facility is backed by Klarna’s receivables portfolio in Germany, a market in which Santander technically competes with Klarna through its own Zinia BNPL offering. Klarna commented on the news, saying that the new facility helps the company diversify its funding sources.

Fifth Third Acquires DTS Connex; Thread Selects Fiserv’s Finxact

Regional powerhouse Fifth Third is bulking up its cash logistics business with the acquisition of software company DTS Connex, the bank announced last week. DTS Connex offers cash management capabilities to health care providers, retailers, and restaurants. The company became a wholly-owned subsidiary of Fifth Third as of August 1st, but will continue to operate independently. Fifth Third’s head of commercial statements said of the deal, “This acquisition expands our ability to automate cash operations and fosters deeper collaboration across the cash ecosystem through advanced data sharing.”

Meanwhile, Tennessee-based Thread Bank announced it has selected Fiserv’s Finxact as the bank’s core banking platform. Thread said that it selected Finxact because its “real-time” core and API-first structure is aligned with the bank’s embedded banking strategy. In addition, Thread will leverage Infinant an embedded banking layer alongside the Finxact core, the bank’s release said.

Elavon to Offer Rev-Based Financing

U.S. Bank’s merchant acquiring unit, Elavon, will begin offering a revenue-based financing option through a partnership with Liberis. The white-label deal allowed Evalon to launch embedding lending capabilities by launching its own branded offering, dubbed Quick Capital. Loan amounts range from as low as $1,000 up to $500,000. CEO of Elavon Jamie Walker explained, “Quick Capital allows our merchants to access capital through a simple, streamlined process and solutions that work with their cash flow, not against it - especially when opportunities or challenges come up unexpectedly.”