Retail Sales Inch Up; Klarna Files F-1; SoFi and Blue Owl Partner

FOMC meets, holds rates steady. Retail sales inch up. Klarna files F-1, drives IPO narrative. SoFi and Blue Owl partner. Is the window for bank charters opening? Affirm to begin furnishing pay-in-four data. Verizon and Santander partner.

Keep an eye out: we will be publishing our Q4 Consumer Lending Review next week. In the meantime, check out our Head of Strategy & Corporate Development, Hillel Olivestone's most recent interview with Current CTO, Trevor Marshall, about owning tech stacks and where bank-fintech partnerships are heading in 2025. Thank you Fintech Business Weekly for having us!

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

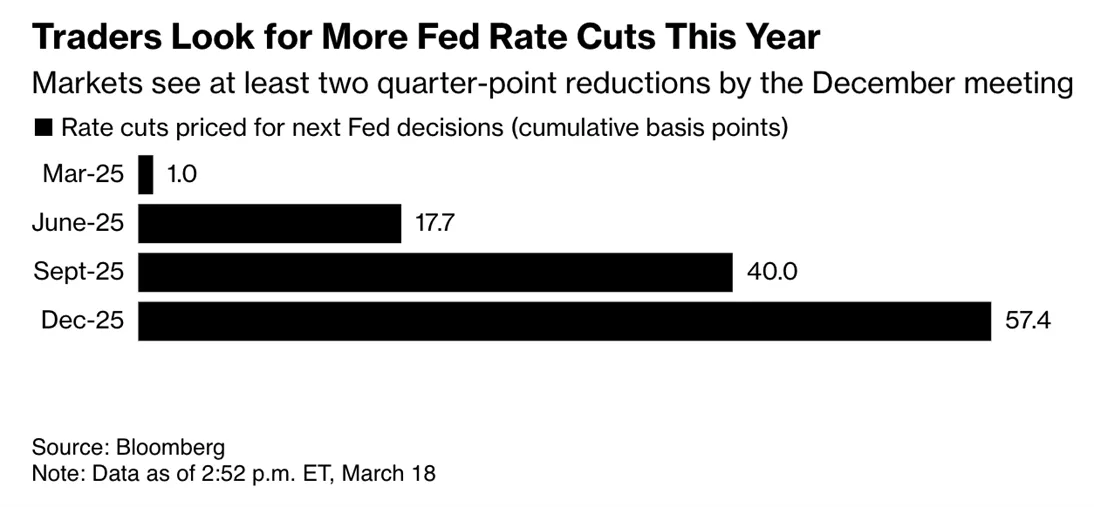

Fed Holds Rates Steady

There are growing concerns that the economy is slowing and inflation is rising, a potentially toxic combination sometimes referred to as “stagflation.” It makes the Fed’s life particularly hard, as the central bank has a dual mandate to support stable prices and promote full employment. At last week’s Fed meeting, the central bank voted to keep rates where they are, in a range of 4.25%-4.5%. Uncertainty about future interest rate movements has been increasing. As of last Tuesday, traders were pricing in approximately two quarter-point rate reductions, down from about three the week prior. Retail sales inched up in February, growing by a less-than-expected 0.2%. Analysts had called for a 0.6% increase.

Klarna Drives Narrative as IPO Approaches

Sweden-based buy now, pay later behemoth Klarna has been busy. The company formally filed its F-1 registration statement with the SEC, as it prepares to go public. The exact price and number of shares has yet to be confirmed. The company plans to list on the NYSE under the symbol “KLAR.” While excitement in the industry is palpable, Klarna may struggle to eclipse its previous high-water market of $46Bn, achieved when it raised a monster $639Mn round led by Softbank. According to the company’s F-1, as of the end of last year, it had 93Mn active users, 675,000 merchants, gross merchandise volume of $2.8Bn, and posted a net profit of $21Mn.

Ahead of the IPO, Klarna is shaping a narrative of growing momentum. Last week, it announced a partnership to power OnePay’s (formerly One) longer-term installment loans, which was widely reported as an “exclusive” with Walmart, though current Walmart BNPL partner Affirm released an 8-K clarifying that, as of now, nothing has changed. OnePay is a separate company majority-owned by Walmart but also counts Ribbit Capital as an investor. Klarna will power loans from 3 months to 36 months in duration for users of OnePay, including for use at Walmart stores.

Perhaps counterintuitively, Klarna has also touted its shrinking headcount, with CEO Sebastian Siemiatkowski leaning in to an AI narrative. Klarna Group’s staff has shrunk by 21% in each of the past two years, as the company has moved to increasingly automate roles, especially in customer support.

Finally, like many other ecommerce and BNPL players, Klarna has been looking to grow a side hustle: advertising. Per its F-1 filing, Klarna earned about $180Mn in 2024 from selling advertising to its merchant clients, or about 6% of the company’s overall revenue.

SoFi Partners with Blue Owl

SoFi has inked a deal with Blue Owl Capital to finance up to $5Bn in personal loans originated through the platform. Blue Owl currently manages about $250Bn of investment funds. SoFi, which became a bank when it acquired Golden Pacific, utilizes various funding sources for its lending, including by originating loans on behalf of third parties. The two-year agreement with Blue Owl should help SoFi increase originations to borrowers it might not otherwise underwrite, while boosting fee-revenue in a capital-light manner.

Is The Window for Bank Charters Finally Open?

With the change of administration, is the window open for fintechs to buy or become banks? That seems to be the conventional wisdom. SmartBiz, once known as BillFloat, announced last week that it has acquired the parent company of Northbrook, Illinois-based Centrust Bank N.A. The Federal Reserve and the OCC approved the transaction. SmartBiz focuses on providing SBA loans. Owning a bank will allow SmartBiz to retain a greater share of the economics from the loans it originates. SmartBiz CEO Evan Singer told Bloomberg, “The main reason we’re doing this is ultimately to serve small businesses really well that aren’t being that well-served today by banks across the country. There’s a huge opportunity to do that.”

Meanwhile, subprime lender OneMain earlier this month announced it had filed applications with the Utah Department of Financial Institutions and the FDIC to establish a wholly-owned industrial bank subsidiary and obtain deposit insurance. To date, OneMain has primarily focused on higher-risk personal and auto lending. According to its release, developing a bank subsidiary would allow OneMain to serve more customers and drive capital generation without significant changes to its capital allocation strategies. OneMain Doug Shulman said, “With a bank subsidiary, we can leverage OneMain Financial’s operational experience and analytic expertise to further expand access to credit to individuals and families, helping them meet today’s needs with a differentiated line of products that provides a path to a better financial future.”

Finally, Cash App, owned by Block, Inc., which also holds an industrial loan company charter, obtained FDIC approval to offer its Cash App Borrow product via its bank subsidiary. Cash App previously offered short-term loans via a partnership with First Electronic Bank. Cash App charges users a flat fee of approximately 5% of the loan, which may be less expensive than other forms of short-term small-dollar credit.

Affirm to Begin Furnishing Pay-in-Four to Experian

While once a hot topic, the discussion around credit reporting for various types of buy now, pay later products has somewhat faded from view. Historically, most BNPL lenders have neither used bureau data to underwrite nor furnished data back to the bureaus for shorter-term pay-in-four products. But, last week, Affirm announced it will begin furnishing data for all of its pay-over-time products to Experian as of April 1st.

Verizon Partners with Santander

Verizon is teaming up with Santander to offer high-yield savings accounts for its mobile phone and 5G home customers. The partnership will leverage Santander’s Openbank platform, which launched in the U.S. last October. Verizon customers can sign up for the offering beginning in April and, in addition to the higher rate on offer from Openbank, also earn Verizon bill credits of up to $180 per year.