Inflation Expectations Ease; New State EWA Laws; DailyPay’s $200MM ABS

Consumers’ inflation expectations ease. Fed officials debate tariffs’ impact on inflation. More states mull EWA laws. DailyPay announces $200MM ABS. Fannie and Freddie to accept mortgages underwritten with VantageScore.

Back in January, our leadership team made their predictions about where fintech was headed. Now, halfway through the year, we’re checking in on where fintech really stands. Join Cross River’s executive panel as we revisit what’s played out, what’s shifted, and what’s next for fintech.

New here? Subscribe here to get our newsletter each Sunday. For even more updates, follow us on LinkedIn.

Consumers’ Inflation Expectations Ease

New data from the Federal Reserve Bank of New York shows that consumer inflation expectations have returned to levels seen at the beginning of the year, before President Trump’s “Liberation Day” tariffs were first announced. A June survey showed the median expectation for price increases one year from year of 3%, marking the second straight month of decreases. The same survey showed mixed views of the labor market. Respondents reported a decreased perceived likelihood of losing their job in the next 12 months, but also indicated they would have a more difficult time finding a new role if they lost their current position, the survey showed.

Meanwhile, minutes of the latest FOMC meeting show officials are divided over the potential for tariffs to impact inflation. “While a few participants noted that tariffs would lead to a one-time increase in prices and would not affect longer-term inflation expectations, most participants noted the risk that tariffs could have more persistent effects on inflation,” the FOMC’s meeting minutes revealed. Still, 10 of the 19 committee members are expecting two rate cuts this year, though seven expect no additional cuts this year. President Trump and members of his administration have stepped up attacks on Fed Chair Powell, arguing he has been too slow to cut rates.

More States Mull EWA Laws

Louisiana has passed an earned wage access law, while Connecticut has sent a bill regulating the industry to the governor for his possible signature. Louisiana became the 11th state to pass legislation specifically addressing EWA. The Louisiana law requires all EWA providers to clearly disclose all fees to users, to allow users to cancel services without cost, to explain how users can file a complaint about services, and to offer a “no cost” option for services, which often entails slower access to funds. The measure also prohibits the repayment of outstanding advances via credit card and does not allow for EWA providers to share fees with a user’s employer. Louisiana’s law further prohibits providers from engaging in false or deceptive advertising. EWA providers will not be considered “lenders” under Louisiana law, as long as they operate consistently with the new law’s requirements.

While Louisiana’s measure is largely in line with the lighter-touch approach favored by industry, the Connecticut bill, not yet passed into law, has raised concerns from industry stakeholders that include an industry trade group, American Fintech Council, as well as EWA providers DailyPay and EarnIn. One concern is around fee caps in the legislation, which would limit fees to a maximum of $4 per transaction and $30 per month for an individual user. “These proposed caps on EWA fees are stricter than any others enacted within the United States, and likely below the fully-burdened cost of operation for many providers,” AFC CEO Phil Goldfeder wrote in a June 25th letter to Democratic Connecticut Governor Edward Lamont. Industry stakeholders also pushed back on a proposed requirement that EWA providers offer at least 75% of an employee’s accrued but unpaid wages, arguing such a requirement would unfairly benefit larger EWA providers. Should the Connecticut bill be finalized as is, it may require some EWA firms to stop operating in the state, industry participants have said.

DailyPay Announces $200MM ABS

Speaking of earned wage access… DailyPay, one of the more established employer-integrated EWA providers, announced a novel asset-backed securitization to enable it to accelerate its growth. DailyPay worked with Barcalys, Citi, and Morgan Stanley on the $200Mn securitization deal, the first such ABS deal in the EWA space. The ABS notes are backed by DailyPay’s EWA receivables. Because in DailyPay’s employer-integrated approach, repayment is coming directly from the user’s employer, loss rates should be much lower than typical unsecured credit extended to the same customer segments. All four tranches of the ABS will trade publicly, according to a DailyPay spokesperson. “This securitization marks a first for our industry, with strong investor demand validating our differentiated approach. With $25 billion in payments volume, we are continuously looking for new ways to optimize our capital structure to support our growth ambitions,” DailyPay CFO Deepa Subramanian commented on the transaction.

Cherry Technologies Closes $420MM ABS

Cherry Technologies, a leading consumer financing platform, closed its second asset-backed securitization, issuing $420 million in notes backed by point-of-sale receivables. The deal — CHRY 2025-1 — was increased by 40% from its original size due to investor demand across all four tiers. Barclays acted as sole structuring agent and joint lead bookrunner, alongside CRB Securities and Truist Securities. CHRY 2025-1 reinforces Cherry’s position in the capital markets and highlights growing interest in embedded finance models.

FHFA Says Fannie, Freddie Can Accept VantageScore 4.0

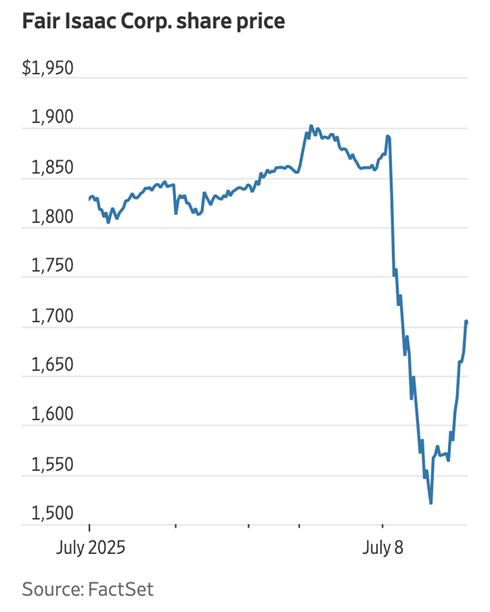

The Federal Housing Finance Authority said that Fannie Mae and Freddie Mac are now permitted to purchase mortgages that lenders have underwritten using VantageScore 4.0, as well as FICO’s 10T model. The development could open up a significant market opportunity for VantageScore, which is owned by a joint venture of the three major credit bureaus, as about half of recently originated mortgages were sold on to Fannie or Freddie. FHFA Director Bill Pulte, an active poster on social media platform X, positioned the change to accept VantageScore as part of a broader effort to reduce mortgage cost and to expand access to mortgage finance, particularly for rural residents and those currently renting. FICO, which has enjoyed a de facto government-granted monopoly for mortgages sold to the GSEs, saw its share price dip by almost 10% on the news.